Charm Industrial

Charm Industrial is a leading durable carbon removal supplier using biomass-to-bio-oil conversion and underground storage. It is relevant carbon-market infrastructure, but it is procurement exposure — not a liquid investment, yield product, or tradable carbon vehicle.

What the data actually shows - TL;DR

Charm Industrial is a durable carbon removal supplier with one of the more validated commercial profiles in the category — visible enterprise buyers, public ledger evidence, and a pathway-specific MRV story — but it is a procurement product, not an investment product. Buyers underwrite delivery execution, evidence quality, and contract enforceability rather than yield or capital appreciation.

Quick Verdict

Is this platform right for you?

Charm Industrial is a leading durable carbon removal supplier with stronger commercial validation and public transparency than most peers in the category, but it is a procurement product, not an investment vehicle. Buyers should evaluate Charm by contract enforceability, MRV scope, evidence package quality, and delivery execution — not by yield or capital appreciation metrics. Don't let brand strength substitute for contract-level diligence.

Best for

- Enterprise climate procurement teams that can negotiate offtake agreements, MRV boundaries, and remediation terms

- Sustainability research and thematic analysis on the durable carbon removal category

- Buyers who value pathway-specific MRV and a public removal ledger as transparency anchors

- Organizations buying carbon removal for retirement and audit-ready claims (not for resale or trading)

Avoid if

- You're an investor seeking yield, capital appreciation, or tradable exposure to carbon removal economics — Charm is procurement, not investing

- Your procurement program requires fully standardized public enterprise pricing or remediation terms — Charm's enterprise economics are negotiated, not posted

- You require SEC primary-source disclosure of capital stack or board composition before counterparty engagement — Charm has no SEC EDGAR footprint

- You need liquid secondary market access for delivered carbon removal — Charm's service-layer terms restrict resale and transfer

Top strengths

- Visible durable carbon removal supplier with named enterprise buyers and Frontier ecosystem validation.

- Public removal ledger creates a stronger activity and transparency signal than most carbon removal operators expose.

- Clear procurement framing reduces confusion with yield-bearing or tradable investment products.

- Public small-buyer plan gives at least one observable pricing reference point, even though enterprise terms remain negotiated.

Key limitations

- Capital stack and ownership transparency: no SEC primary-source filings; Charm's investors and board composition are not documented in EDGAR.

- Enterprise pricing transparency: public pricing only for small-buyer plans; enterprise economics are negotiated and not publicly posted.

- Contract enforceability: public web terms include arbitration, no-warranty, and restrictive transferability language; actual enterprise offtake contracts may differ but are not publicly accessible.

- Buyer concentration: revenue base is structurally tied to Frontier-aligned corporate sustainability programs (Stripe, Alphabet, Microsoft, Meta, Shopify, McKinsey ecosystem).

Compare Before Deciding

Where Charm Industrial fits against alternatives

Use these hooks to pressure-test whether this is the right platform, or whether a nearby alternative matches the job better.

How this compares to Carbonfuture

Carbonfuture

Carbonfuture is procurement and MRV infrastructure across suppliers, while Charm is a direct removal supplier with a proprietary pathway.

How this compares to Patch

Patch

Patch is broader procurement infrastructure, while Charm is supply-side carbon removal production and delivery.

Why It Matters

Investor relevance and market role

Charm is worth tracking because it is a leading supply-side carbon removal operator with real enterprise buyers, visible delivery activity, and stronger market credibility than many concept-stage climate projects. For most AltStreet readers, the key point is not direct investability but thematic relevance: Charm helps validate durable carbon removal as a real market, while investor access usually has to come through adjacent funds, marketplaces, or infrastructure businesses rather than through Charm itself.

Type

Carbon removal operator (infrastructure)

Access

Not available as a public retail investment

Role

Supply-side carbon credit generation and delivery

Investor Relevance

Theme signal and ecosystem bellwether, not direct portfolio access

Real-world validation

- Charm publicly lists major buyers and partners including Frontier, Stripe, Alphabet, Shopify, Meta, JPMorgan Chase, H&M Group, Workday, and Microsoft.

- The homepage and solutions pages position Charm as an enterprise supplier already working with named climate buyers rather than as a concept-stage startup with only theoretical demand.

- The dossier surfaced Frontier's first $53 million of offtake agreements with Charm as a featured credibility signal.

- Public ledger and MRV positioning give buyers a stronger validation trail than a generic offset storefront.

Scale signals

Public ledger activity

13,063 tonnes CO2e

Homepage-linked total tonnes of carbon dioxide removed per AltStreet's April 18, 2026 ledger snapshot.

Offtake signal

$53 million

Featured Frontier offtake reference surfaced in the June 18, 2026 dossier.

Capital signal

$100 million Series B

Company blog reference surfaced in the June 18, 2026 dossier set.

How investors can engage the theme

Charm itself is better treated as ecosystem context than as a directly investable security. If your goal is portfolio exposure to carbon removal, the practical question is where capital can actually access the theme, not whether you can buy Charm tons like a liquid asset.

- Carbon marketplaces and procurement platforms that give operational exposure to the carbon removal ecosystem.

- Private funds, venture vehicles, or project-finance structures focused on climate infrastructure and carbon removal supply.

- Public-market climate and industrial infrastructure businesses that may benefit as carbon removal supply chains scale, even if they are not pure-play Charm equivalents.

Quick Answers

What most investors want to know first

The highest-signal facts first: minimums, liquidity reality, K-1 timing, and whether distributions are actually part of the experience.

Liquidity

Charm should not be described as a trading venue or liquid carbon-investment market. The updated dossier did not surface a public secondary market; the strongest public signal is restrictive no-resale / non-transfer language around service use. The best-supported narrower inference is that some enterprise buyers may receive contractual transfer rights in delivered tons, which is operational flexibility rather than market liquidity.

K-1 Timing

No K-1 or investor-style tax document workflow was identified in the June 18 2026 dossier set. Charm appears to operate as a carbon-removal procurement service rather than an investment vehicle.

Distributions

Not applicable in the investment sense. Platform materials focus on purchase, delivery, retirement, and evidence rather than cash payouts to users.

Overview

Platform Overview

A concise read on what the platform is, how the structure works, and where the practical friction shows up for real investors.

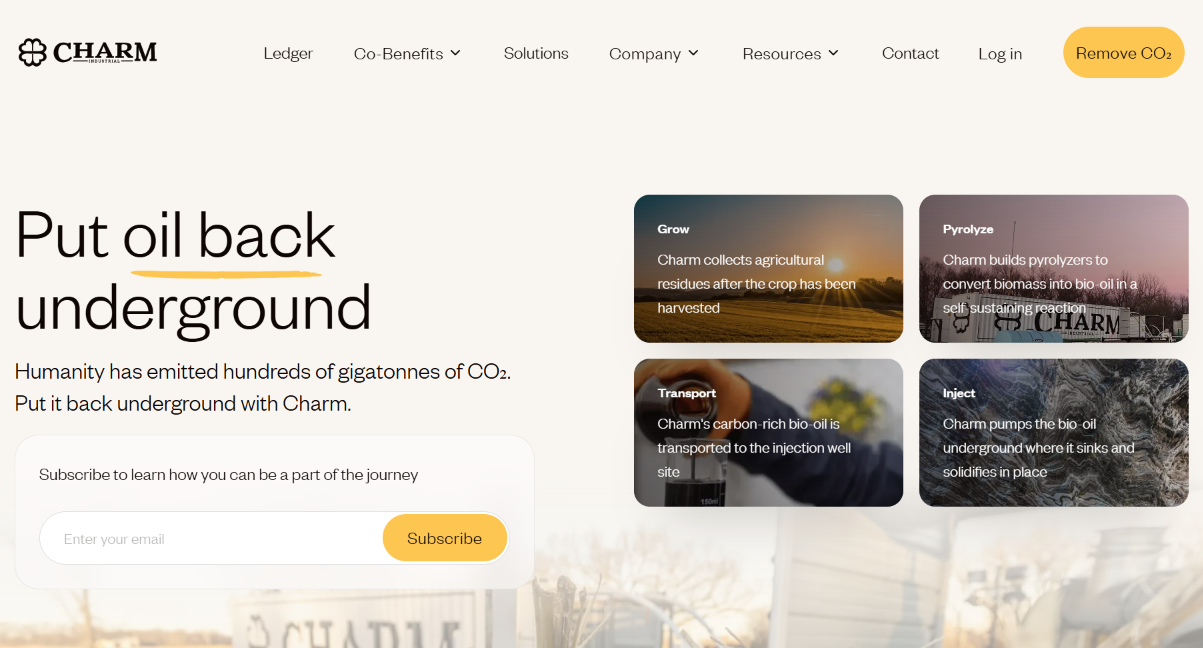

Charm Industrial delivers durable carbon removal by converting biomass residues into bio-oil and storing it underground, then selling the associated removal through enterprise offtake and smaller buyer purchase workflows with monitoring, reporting, verification, and retirement evidence as the core claim layer.

According to platform materials and the June 18 2026 dossier set, Charm is a direct durable carbon removal supplier centered on biomass-to-bio-oil conversion and underground injection. The platform is primarily enterprise-oriented, but the updated dossier also shows a public small-buyer plan flow with monthly pricing and a sales-assist threshold for larger orders. This is still procurement infrastructure, not an investment product: the critical diligence issues are MRV boundaries, delivery evidence, durability assumptions, and whether the executed purchase documents provide meaningful remedies, title transfer rights, and evidence packages if delivery or verification goes wrong.

Platform Model

Direct Supplier / Project Developer

Primary Function

Durable Carbon Removal Delivery

Target Users

Enterprise buyers, aggregators, and some small buyers

Commercial Lens

Offtake + purchase plans + MRV evidence

ASHow It Works

- Charm sources biomass residues, converts them into bio-oil, transports the output, and injects it underground as the core removal pathway.

- The public ledger creates a stronger transparency signal than the older review captured by surfacing current removal activity.

- Enterprise demand appears central, with prominent customer references and enterprise solution pages, but there is also a public consumer / small-business plan flow.

- Public pricing is partial: the plans page shows a $30.00 per month option for 50kg CO2e per month and states that orders above $5,000 require sales assistance.

- The research also supports a more formal enterprise stack with multi-year offtakes, tiered pricing logic, ton-level remediation concepts, and detailed audit evidence expectations, even though the actual contract language is not public.

- Because this is procurement rather than investing, the real economic protection still lives in the executed purchase or offtake agreement, not in web copy.

Key Gaps & Non-Disclosures

- Full enterprise price schedules and volume-discount mechanics are not publicly posted

- Public web materials do not fully explain ton-level remediation or replacement obligations

- Post-issuance invalidation, reversal, or methodology-change treatment remains contract-dependent

- Public transferability language is mostly restrictive and refers to service use; enterprise asset-transfer rights may exist, but they are not publicly documented in full contract form

Platform Intelligence

Charm Industrial Timeline

Key platform events, regulatory turns, liquidity stress points, and product launches that shape how the review should be read.

Charm Industrial founded

Peter Reinhardt (former Segment co-founder) and team incorporate Charm Industrial in San Francisco to commercialize biomass-to-bio-oil durable carbon removal.

Frontier $53M offtake commitment

Frontier (the advance market commitment fund founded by Stripe, Alphabet, Meta, Shopify, and McKinsey) publicly discloses an initial $53M offtake commitment to Charm Industrial. This becomes a major external validation channel for Charm's commercial profile. AltStreet has not independently verified the specific deal terms beyond Frontier's published disclosure.

$100M Series B (per company blog)

Charm Industrial publicly announces a $100M Series B funding round via the company blog. AltStreet has not located a corresponding SEC Form D filing in EDGAR; the round's specific investors, valuation, and capital structure are not documented in SEC primary filings.

Enterprise customer roster expands

Charm's public materials surface a broader enterprise customer set including Stripe, Alphabet, Microsoft, Shopify, Meta, JPMorgan Chase, H&M Group, and Workday. AltStreet has not independently verified the individual offtake terms for each.

Public ledger snapshot: 13,063 tonnes removed

AltStreet's April 18, 2026 ledger snapshot captures Charm's public removal ledger at a platform-reported cumulative total of 13,063 tonnes of CO2e removed. The public ledger is one of the stronger transparency signals in the durable carbon removal category, though buyers should validate individual delivery records against their own evidence package.

AltStreet snapshot: no SEC EDGAR footprint

AltStreet conducts three SEC EDGAR Form D searches against Charm Industrial entity name variations on June 18, 2026. All return zero matches. AltStreet did not identify SEC primary-source filings for Charm Industrial in these searches, consistent with the company being a carbon removal supplier rather than a securities issuer.

Investor Operations

The practical questions investors actually care about: when tax documents arrive, how cash distributions work, and whether capital can be exited before the underlying asset is sold.

Tax Documents

K-1 Timing

What to expect

No K-1 or investor-style tax document workflow was identified in the June 18 2026 dossier set. Charm appears to operate as a carbon-removal procurement service rather than an investment vehicle.

Delay signals

- The enhanced dossier explicitly notes that no tax reporting or form issuance was referenced in available materials.

Extension risk

No extension-related investor tax workflow was identified. Buyers should instead expect ordinary internal accounting treatment of procurement spend, subject to jurisdiction and contract structure.

Confidence: High

Cash Flow

Distributions

Frequency

No dividend, yield, or investor distribution schedule was identified. Charm is not presented as an income-producing investment platform.

Timing

Not applicable in the investment sense. Platform materials focus on purchase, delivery, retirement, and evidence rather than cash payouts to users.

Consistency

Not applicable. Economic value flows through contracted removal delivery rather than periodic investor distributions.

Confidence: High

Liquidity

Exit Reality

Holding period

No investor lockup framework was disclosed because Charm is not presented as an investment vehicle. Buyers may face contractual commitment duration through subscriptions, forward purchases, or enterprise offtake terms, but that is procurement lock-in rather than investor lockup.

Exit options

- No investor redemption workflow was identified for Charm users.

- The public plans page indicates a small-buyer recurring purchase flow, but not a resale or redemption mechanism.

- Public terms language includes no-resale and non-transfer restrictions for the service layer, which is the opposite of open secondary liquidity.

- Research suggests some enterprise contracts may allow reassignment or transfer of delivered tons after title vests, but that is contract-governed asset administration rather than a public market exit.

Secondary market

Charm should not be described as a trading venue or liquid carbon-investment market. The updated dossier did not surface a public secondary market; the strongest public signal is restrictive no-resale / non-transfer language around service use. The best-supported narrower inference is that some enterprise buyers may receive contractual transfer rights in delivered tons, which is operational flexibility rather than market liquidity.

Confidence: Medium

Investment Structures

Charm does not offer a securities-style investment product. Buyers purchase durable carbon removal for retirement, climate claims, and reporting rather than for yield, dividends, or capital appreciation.

- No stated return profile or yield mechanics

- No public secondary market or redemption path for investors

- Economic exposure is tied to delivery, evidence quality, and contract performance

- Any transfer or claim treatment is contract-defined, not exchange-defined

Risk

Risk Structure

This is where the marketplace pitch gives way to the actual operating reality: delayed exits, limited disclosure, fee drag, and path-dependent outcomes.

No SEC EDGAR primary-source footprint

AltStreet's June 18, 2026 search across multiple Charm Industrial entity name variations returned zero matches in EDGAR for Form D and all other SEC form types. This is consistent with Charm being a carbon removal supplier rather than a securities issuer. The absence likely reflects private financing conducted through pathways that did not generate public SEC filings — such as reliance on Section 4(a)(2), Regulation S, state-law exemptions, or other private-offering pathways. The structural implication is that Charm's capital stack, ownership composition, board membership, and investor identities are not documented in publicly accessible SEC primary filings (though some of these details may be documented in press releases, company materials, or third-party databases). Diligence must rely on Charm's own published materials, ecosystem disclosures (Frontier, customer 10-Ks), and direct counterparty research.

Direct Supplier Exposure

Charm is a direct removal provider, so buyer risk centers on operating execution, feedstock sourcing, process uptime, injection operations, and whether delivered tons meet the contracted evidence standard.

MRV & Claims Boundary

The value of the purchase depends on what is measured, what is modeled, how permanence is defined, and what evidence the buyer can retain for audit and disclosure purposes.

Partial Pricing Transparency

The updated dossier improves pricing visibility for small buyers with a public monthly plan and a sales-assist threshold above $5,000, but enterprise price discovery still appears negotiated rather than transparent.

Legal Terms Visibility

The updated dossier now identifies terms and conditions plus privacy policy pages, and the enhanced analysis flags arbitration, no-warranty language, and transfer restrictions. The research adds a stronger enterprise-law frame around governing law, arbitration, indemnity, hierarchy of terms, and ton title vesting, but that still does not replace actual contract review.

Delivery Shortfall / Timing Risk

Risk Summary

Multi-year or forward purchases can miss contracted timing or volume because supply, operations, or verification processes slip.

Why It Matters

Buyers often tie removals to reporting cycles and public climate commitments. Delivery delays can create procurement gaps and claims problems.

Mitigation / Verification

Require milestone-based delivery schedules, acceptance criteria, and written remedies for late or short delivery, including replacement tons, refunds, or other make-goods.

Contract Split / Hierarchy Risk

Risk Summary

The public service terms and the enterprise asset purchase logic may differ materially, especially on transferability, liability caps, and dispute procedures.

Why It Matters

If hierarchy-of-terms is unclear, a buyer may assume delivered tons are transferable or fully protected when the operative contract says something narrower or routes disputes differently.

Mitigation / Verification

Require a written hierarchy of terms showing whether the master purchase or offtake agreement supersedes public website terms for liability, transferability, remedies, and dispute resolution.

MRV / Methodology Change Risk

Risk Summary

Verification frameworks and methodological expectations can tighten over time, creating disputes over already-contracted or already-delivered tons.

Why It Matters

A buyer may pay for delivery but still lose some intended reporting or reputational value if standards shift.

Mitigation / Verification

Request change-control language covering re-verification cost, updated evidence requirements, and responsibility if methodologies or registries change.

Weak Public Remedy Clarity

Risk Summary

Public web materials still do not spell out a universal remediation policy for invalidation, reversal, or post-issuance disputes.

Why It Matters

If remedies are unclear, the buyer can end up carrying reputational and compliance risk in the exact scenarios that matter most.

Mitigation / Verification

Request a scenario-based remedy schedule covering delivery failure, invalidation, dispute, and alleged reversal events before signing.

No-Resale / Low-Liquidity Reality

Risk Summary

The public web flow includes restrictive no-resale and non-transfer language for the service layer, and no public secondary market surfaced in the dossier. Research does support a narrower possibility that delivered enterprise tons can be reassigned or transferred by contract after title vests, but that is not the same as broad market liquidity.

Why It Matters

Buyers should not assume easy liquidity. Even if enterprise contracts permit reassignment of delivered tons, that is an operational asset-transfer right, not a public trading market.

Mitigation / Verification

Clarify in writing whether delivered tons, attestations, or credits can be reassigned, transferred, or re-designated under enterprise contracts, and whether any approvals, registry updates, or ledger reissuance steps apply.

ASRisk signals to watch

- Material changes to Charm's public removal ledger reporting cadence or methodology

- Updates to Charm's terms of service materially expanding or restricting service-layer transferability

- Charm SEC filings appearing in EDGAR (would indicate a shift toward securities-issuer structure, possibly IPO preparation)

- Frontier disclosure updates on Charm offtake performance, deliverables, or contract amendments

- Customer 10-K disclosures from Stripe, Alphabet, Meta, Microsoft, or others materially expanding or reducing Charm offtake commitments

Biggest Misconceptions & What Actually Happens

- What contractual framework governs ton-level warranties, remediation, and replacement obligations for delivered carbon removal?

- Does the executed enterprise agreement supersede public web terms for liability caps, transferability, and dispute resolution?

- What is the underwriter's responsibility for re-verification cost and updated evidence if methodologies or registries change post-delivery?

- What evidence package — monitoring records, verification artifacts, retirement attestations — is contractually delivered alongside the tons?

- Are delivered tons or attestations reassignable under enterprise contracts, and what registry or ledger update steps apply?

Regulatory & Legal Posture

Security Status

Procurement Product / Not Securities-Style Access

Charm's core activity, as observable from public materials and the June 18 2026 dossier, is supplying durable carbon removal for procurement, retirement, and claims workflows rather than issuing securities or pooling capital for financial returns. AltStreet has reviewed only public web flows and not enterprise contract documents; carbon removal rights can be legally nuanced depending on how they are packaged, financed, resold, tokenized, pooled, or marketed..

Disclosure Quality

Moderate. The updated dossier improves visibility into public legal pages, pricing snippets, and operational posture, and the research supports more enterprise-grade legal architecture, but the operative contractual protections still are not fully public.

Custody Model

No Traditional Investment Custody

Regulatory Backing

Charm functions as a supplier and service provider rather than a custodian of investor assets. Any transfer, retirement, or evidence treatment for delivered removals depends on the purchase structure, verification pathway, title-vesting mechanics, and executed buyer agreement rather than on platform custody rules..

Tax Treatment

Reporting

Not Applicable

Carbon removal purchases on Charm are presented as procurement rather than investment activity. The enhanced dossier explicitly notes that no tax reporting or form issuance was referenced in available materials, so standard investment tax forms are generally not expected from the platform itself.

Income Character

Business Expense / Procurement

Purchases are made to retire removals, support climate claims, or meet sustainability objectives rather than to generate yield or investment income..

Limitation

Tax and accounting treatment can vary by jurisdiction, buyer structure, and whether removals are retired internally or used in another commercial workflow. Consult tax and accounting advisors for your specific treatment.

Before You Invest

Get Charm Industrial investor insights before you invest

K-1 timing, distribution updates, yield insights, and risk signals for Charm Industrial and similar platforms.

- Weekly platform research focused on tax timing and liquidity reality.

- Signals on distributions, risks, and structural tradeoffs before capital is locked up.

- Coverage of adjacent platforms so you can compare better options faster.

Get weekly platform signals

Track fee changes, liquidity updates, risk flags, and adjacent platforms before you invest.

Independent intelligence from AltStreet. No hype. No sponsor spin.

AltStreet Data Layer

What the data actually shows

AltStreet's June 18, 2026 Charm Industrial review combines public site materials, public ledger observations, enhanced contract-risk synthesis, and SEC EDGAR search results. Key findings from the data layer:

Procurement-only commercial model with zero SEC primary-source footprint

Three SEC EDGAR Form D searches against Charm Industrial entity name variations on June 18, 2026 returned zero matches. No 10-K, 10-Q, S-1, Form 1-A, Form C, or any other SEC filing exists for Charm Industrial.

What this means

Charm's capital stack, board composition, and investor identities are not documented in publicly accessible SEC primary filings (though some of these details may be documented in press releases, company materials, or third-party databases). This is structurally consistent with a non-securities-issuer model. The absence of SEC filings likely reflects private financing conducted through pathways that did not generate public SEC filings, such as reliance on Section 4(a)(2), Regulation S, state-law exemptions, or other private-offering pathways. Buyers diligencing Charm should rely on the company's own published materials, Frontier ecosystem disclosures, customer 10-K mentions, and direct counterparty research rather than SEC filings.

Public ledger transparency appears stronger than category average

Charm publishes a public removal ledger with cumulative tonnes (13,063 CO2e as of April 18, 2026 snapshot) and operational delivery activity. This is more transparency infrastructure than most carbon removal operators expose publicly.

What this means

The public ledger is a meaningful diligence asset — it provides a verifiable activity signal independent of marketing claims. Buyers should still validate individual delivery records against their own evidence package and the contracted MRV scope, but the public ledger is a stronger transparency baseline than most peers offer.

Buyer concentration in Frontier-aligned corporate climate programs

Charm's publicly disclosed customer roster (Frontier, Stripe, Alphabet, Microsoft, Shopify, Meta, JPMorgan Chase, H&M Group, Workday) overlaps substantially with Frontier's founding members and their broader corporate climate procurement ecosystem.

What this means

Charm's revenue appears structurally tied to the Frontier-adjacent corporate sustainability procurement ecosystem. If Frontier or its founding members materially reduce carbon removal procurement spend (due to budget pressures, sustainability strategy shifts, or regulatory changes), Charm's revenue base is concentrated rather than diversified across asset classes. Buyer concentration appears to be a major economic exposure.

Partial public pricing transparency

Charm posts a public small-buyer plan at $30/month for 50kg CO2e and a sales-assist threshold above $5,000, but enterprise pricing schedules, ton-level remediation costs, and volume discount mechanics are not publicly posted.

What this means

Small-buyer pricing transparency is better than most carbon removal operators. Enterprise pricing is negotiated and not standardized — material pricing variability is likely across buyers. Enterprise procurement teams should not assume the public plan price translates to enterprise per-ton economics; the per-ton economics at scale are likely materially different.

Data as of 2026-06-18 . AltStreet review evidence layer . Public-source analysis

Decision Fit

Investor Fit

Who this works for, who it does not, and what level of patience and complexity tolerance the platform really demands.

Institutional / Enterprise Buyers

Best fit for enterprise climate procurement teams that can negotiate contracts, evaluate MRV boundaries, manage delivery and remediation terms, and maintain evidence for public claims over time..

ESG / Climate SaaS Providers

Potential fit where an intermediary or program manager wraps Charm supply into a broader workflow, but public API and standardized partner documentation were not strongly surfaced in the dossier..

Retail / Individual Investors

The updated dossier shows a public consumer / small-business plan flow, so Charm is not enterprise-only. But the product is still not a liquid consumer asset, and larger orders quickly move into higher-touch sales assistance..

Investors Seeking Financial Returns

Charm is procurement plus delivery evidence, not a carbon investment vehicle. If you want tradable exposure or yield, this is the wrong structure..

Tradeoffs

Key Tradeoffs

The attraction of pre-IPO access is real, but every benefit comes bundled with a corresponding liquidity, transparency, or pricing cost.

Durability vs Simplicity

Charm's durable pathway can support stronger claims than generic offsets, but requires more diligence and usually more contract negotiation..

Direct Supplier Exposure vs Marketplace Optionality

Working with a direct supplier can improve pathway visibility, but gives buyers less diversification and less sourcing flexibility than a broad marketplace..

Some Public Pricing vs Limited Enterprise Transparency

The updated dossier improves price visibility for smaller buyers, but enterprise pricing and remedies still appear negotiated rather than standardized..

Avoid

Who This Is Not For

This section should be read as a filter, not an afterthought. If you need income, simplicity, or near-term access to capital, the structure is working against you.

Investors Seeking Financial Returns

Charm is not an investment product. It is a procurement workflow for durable carbon removal, with no yield, dividend, or public trading mechanism..

Buyers Requiring Liquidity

The updated dossier surfaced restrictive no-resale and non-transfer service language, not a public secondary market or redemption path. Even where enterprise contracts may allow asset reassignment, that is not equivalent to liquid resale..

Teams Without Diligence Capacity

Buyers still need to understand MRV boundaries, contract remedies, and claims governance. Without that capability, durable removals can create compliance and reputational risk..

Editorial View

AltStreet Perspective

The compressed version of the review: what matters, what marketing tends to obscure, and how we would frame the platform for a serious allocator.

Verdict

Charm is a leading durable carbon removal operator and a meaningful signal for the carbon removal market, but it is not a direct investment product and the real buyer risk still lives in the contract and evidence package.

Positioning

Most compelling for enterprises that want direct exposure to a specific durable-removal pathway and are prepared to negotiate delivery, evidence, title-transfer, and remedy terms. For investors, Charm is better used as a market signal and diligence anchor than as a direct access point. The June 18 2026 dossier also shows a public small-buyer plan flow, so Charm is broader commercially than a pure enterprise-only supplier, but it still is not an investment or trading venue.

The Bottom Line

Track Charm to understand carbon removal market maturity; buy it for procurement if needed, but seek thematic investment exposure elsewhere.

Action

Next Steps

If you still want to engage after reading the review, these are the practical next moves that reduce avoidable mistakes.

Request a written remediation schedule covering short delivery, invalidation, methodology change, and any alleged reversal event.

Validate the evidence package you will receive: monitoring records, verification artifacts, retirement or attestation proofs, and claims-use guidance.

Clarify hierarchy of terms: confirm whether the executed enterprise agreement supersedes restrictive public web terms for disputes, liability, and ton-level remedies.

If you are buying at enterprise scale, request a full numeric pricing breakdown rather than relying on the public small-buyer plan page.

Confirm whether delivered removals, attestations, or related claims can be reassigned or transferred under your contract if your internal program changes, and what registry or ledger steps are required.

Appendix

Sources, Disclosures, and Supporting Context

The lower section is structured like a report appendix: relationship context first, adjacent reading second, and evidence last.

Report Appendix

Disclosure

Relationship and compensation context

+

Report Appendix

Disclosure

Relationship and compensation context

Report Appendix

Related Resources

Adjacent platform comparisons, frameworks, and category links

+

Report Appendix

Related Resources

Adjacent platform comparisons, frameworks, and category links

Further Reading

Related Resources

Adjacent frameworks and reviews that help place the platform in a broader allocation or due-diligence context.

Explore Asset Class

Carbon & ClimateFrameworks

Similar Platform Reviews

- Carbonfuture

Carbonfuture is procurement and MRV infrastructure across suppliers, while Charm is a direct removal supplier with a proprietary pathway.

- Patch

Patch is broader procurement infrastructure, while Charm is supply-side carbon removal production and delivery.

Report Appendix

Evidence & Methodology

Sources, scope, and how the review was assembled

+

Report Appendix

Evidence & Methodology

Sources, scope, and how the review was assembled

ASReview Evidence

Methodology

June 18 2026 Firecrawl dossier plus enhanced synthesis plus public Charm Industrial pages including homepage, plans, solutions, FAQ, ledger, terms and conditions, and privacy policy, supplemented by structured analysis of enterprise contract diligence areas (offtake architecture, remediation, transferability, pricing, evidence rights). AltStreet conducted three SEC EDGAR Form D searches against Charm Industrial entity name variations on June 18, 2026; all returned zero matches across all SEC form types. AltStreet did not identify SEC primary-source filings for Charm Industrial in those searches, consistent with the company's carbon removal supplier model rather than a securities-issuer model.

Scope

June 18 2026 dossier JSON and enhanced dossier analysis plus public site materials covering product pathway, enterprise solutions, consumer plans, legal pages, and public removal ledger, supplemented by structured analysis of likely enterprise contract diligence issues (ton-level remediation, title vesting, pricing tiers, audit evidence package). AltStreet's SEC EDGAR search returned no Charm Industrial filings; the review therefore does not include SEC primary-source evidence.

Key Findings

- *PLATFORM-CONFIRMED: Charm is positioned as a direct durable carbon removal supplier built around biomass-to-bio-oil conversion and underground injection.

- *PLATFORM-CONFIRMED: The homepage and solutions pages reinforce enterprise demand and showcase large named buyers and offtake credibility.

- *PLATFORM-CONFIRMED: The plans page shows a public small-buyer pricing signal of $30.00 per month for 50kg CO2e per month and states that orders above $5,000 require sales assistance.

- *PLATFORM-CONFIRMED: The homepage links to a public ledger and surfaced 13,063 total tonnes of carbon dioxide removed as of April 18, 2026.

- *PLATFORM-CONFIRMED: Charm publicly showcases major buyers and partners including Frontier, Stripe, Alphabet, Shopify, Meta, JPMorgan Chase, H&M Group, Workday, and Microsoft.

- *PLATFORM-CONFIRMED: Terms and conditions and privacy policy pages are publicly discoverable in the updated dossier.

- *PLATFORM-CONFIRMED ABSENCE: Enhanced dossier notes that no tax reporting or form issuance was referenced in available materials.

- *STRUCTURAL FINDING: AltStreet's June 18, 2026 SEC EDGAR search across multiple Charm Industrial entity name variations returned zero matches. AltStreet did not identify SEC primary-source filings for Charm Industrial in those searches.

- *LEGAL-SIGNAL: Enhanced analysis flags arbitration language, no-warranties language, and restrictive transferability language in the public legal materials.

- *RESEARCH-SUPPORTED: Enterprise framework appears to include more formal offtake-style legal architecture, hierarchy-of-terms logic, ton-level remediation concepts, and detailed audit evidence expectations than the public web materials show.

- *ECOSYSTEM-SOURCED: Featured references include Frontier's first $53 million in offtake agreements and a company blog reference to a $100 million Series B. AltStreet has not independently verified the specific terms of either.

- *RESEARCH-SUPPORTED: Public terms language includes no-resale and non-transfer restrictions for the service layer, but research suggests some enterprise contracts may still permit reassignment or transfer of delivered tons after title vests.

Primary Source Pages

Comparable Platforms

- Carbonfuture

Infrastructure and marketplace layer across suppliers versus Charm as a direct supplier.

- Patch

Broader procurement orchestration versus Charm's pathway-specific direct supply.

FAQ

Frequently Asked Questions

High-intent search questions answered directly, without making users hunt through the full review.

Is Charm Industrial an investment platform?

No. Charm is a carbon removal operator and procurement supplier for durable removals. Buyers purchase removals and evidence for climate claims and reporting, not a return-bearing investment product.

Why should investors care about Charm if they cannot invest directly?

Charm is useful as a market signal. It shows what credible carbon removal supply looks like: named enterprise buyers, live delivery activity, pathway-specific MRV, and real offtake demand. That makes it relevant for understanding the carbon removal theme even if portfolio access usually has to come through adjacent funds, marketplaces, or infrastructure businesses instead of Charm itself.

Does Charm Industrial have public pricing?

Partially. The June 18 2026 dossier surfaced a public plans page showing a $30.00 per month option for 50kg CO2e per month and noted that orders above $5,000 require sales assistance. The research also supports enterprise pricing tiers and declining forward pricing logic, but not a fully public buyer-ready enterprise price schedule.

Does Charm issue K-1s or other investor tax forms?

No investor-style tax workflow was identified in the updated dossier. The platform is framed as carbon-removal procurement rather than investing, so standard investment tax forms are generally not expected from Charm itself.

Can buyers resell or exit positions easily?

Not through a public market. The updated dossier did not surface a public secondary market, and the public legal materials include no-resale and non-transfer service language. The research does suggest that some enterprise contracts may allow reassignment or transfer of delivered tons after title vests, but that is contract-governed asset administration rather than open-market liquidity.

What should enterprise buyers verify before signing?

Verify: (1) delivery timing and shortfall remedies, (2) MRV boundaries and evidence outputs, (3) treatment of invalidation or methodology changes, (4) whether enterprise agreements supersede the public web terms, (5) any transfer or reassignment rights if your internal program changes, and (6) the retention and audit rights attached to the underlying evidence package.

Does Charm Industrial have SEC filings I can review?

No. AltStreet conducted three SEC EDGAR Form D searches against Charm Industrial entity name variations on June 18, 2026; all returned zero matches. AltStreet did not identify SEC primary-source filings for Charm Industrial in those searches. This is consistent with Charm being a carbon removal supplier rather than a securities issuer — capital rounds likely reflect private financing conducted through pathways that did not generate public SEC filings, such as reliance on Section 4(a)(2), Regulation S, state-law exemptions, or other private-offering pathways. The structural implication for buyers is that Charm's capital stack, board composition, and investor identities are not documented in publicly accessible SEC filings (though some of these details may be documented in press releases, company materials, or third-party databases); diligence relies on Charm's own materials, Frontier ecosystem disclosures, and customer 10-K mentions instead.