Percent

Percent reports a 0.90% charge-off rate on its public track record page. AltStreet's full-platform ingest of all 1,067 deals finds something the public page doesn't surface: 49 deals in active workout and 2 reperforming after prior default. The realized charge-off rate is accurate. The lifetime distress rate — workouts, charge-offs, and recoveries combined — is 5.90%. Both numbers matter; only one is visible.

What the data actually shows - TL;DR

Percent is the most institutionally-credible private credit marketplace available to accredited retail: SEC-registered broker-dealer since August 2023, FINRA member, three years of compliant X-17A-5 FOCUS Report filings, $1.93B funded across 1,067 deals, 60,000+ investors, and a self-reported 0.90% charge-off rate that AltStreet's $-weighted analysis confirms at 1.17%. The platform's edge versus competing private credit marketplaces is real — structured Credit Snapshot rubrics, deal-level surveillance reports, third-party underwriter disclosures, and the new (Feb 2026) secondary market. The friction point: deal-state transitions like Workout and Reperforming exist in the investor-api but are not surfaced on the public deal page UI. The headline charge-off rate is accurate. The lifetime distress rate, which includes deals in active workout, is 5.90% — not visible on the deal-by-deal interface.

AltStreet tracks all 1,067 Percent deals via authenticated /investor-api capture (directory + body + borrower endpoints, 2026-05-29), plus Percent's own /our-track-record-of-performance disclosures (3/31/26), plus SEC EDGAR for Percent Securities LLC (CIK 0001863789, X-17A-5 FOCUS Reports FY2023-FY2025).

What's Actually Happening

In plain English, here is what is actually happening.

- 1You are lending money to private companies (or their loan books) for 6-36 months at high interest rates — typically 14-18% annualized coupons.

- 2Percent acts as the broker-dealer arranging each loan, packaging it as a structured note inside its own LLC, and selling slices to you and other accredited investors at $500 minimums.

- 3You receive monthly interest payments. Percent retains 10% of that interest as its servicing fee, so a 16% headline coupon means roughly 14.4% net to you.

- 4Most deals are asset-based — the loan is backed by inventory, receivables, equipment, or merchant cash advances. Some are corporate loans backed only by the borrower's credit.

- 5When deals go bad, you may see partial recovery (workout), full recovery after delay (reperforming), or partial loss (charge-off). On the platform's history, 0.90% of deals end in charge-off — low relative to many public high-yield default benchmarks, though methodologies are not directly comparable.

Quick Verdict

Is this platform right for you?

Percent gives accredited investors institutional-grade private credit access with a $500 minimum, monthly distributions, and a registered broker-dealer wrapper that most marketplace competitors lack. The credit performance is genuinely strong: $1.93B funded across 1,067 deals (793 repaid as of Percent's 3/31/26 disclosure; 801 repaid in AltStreet's 5/29/26 ingest), 0.90% charge-off rate by Percent's methodology (1.17% by AltStreet's $-weighted measure). The friction is that distress states (Workout, Reperforming) exist in the underlying API but are not displayed on the public deal-page UI — and distress concentrates dramatically by financing type (Corporate Loan 25.35% vs Asset-Based 3.79%) and by third-party underwriter (Aluna Partners 33.33% vs Percent self-underwritten 2.59%). The platform is well-suited for accredited investors with $25K-$100K building a 20-deal diversified portfolio across asset-based deals, sized by underwriter quality and deal type.

Best for

- Accredited investors with $25K-$100K seeking diversified private credit exposure through 20-50 deals across multiple borrowers and asset types

- Investors prioritizing short-duration credit (6-36 months) over multi-year private equity-style commitments to capture current high coupon rates

- Investors comfortable evaluating deal-level credit metrics (overcollateralization, simple loss coverage, TTM default rate) on a per-deal basis

- RIAs and family offices with $1M+ allocating via Percent's Separately Managed Account product (1% annual management fee on committed capital)

Avoid if

- You need genuine liquidity within 12 months — the secondary market (Feb 2026 launch) is too new to depend on for guaranteed exit

- Your available capital is under $5K — meaningful diversification across 10+ deals requires $5K-$10K minimum, and concentration risk on single deals is binary

- You hold significant taxable assets in high-tax states — ordinary interest income at 50%+ effective tax rates dramatically erodes the headline 14-18% coupon

- You want passive set-and-forget exposure — marketplace deals require ongoing evaluation of new offerings, monitoring, and reinvestment decisions

Top strengths

- FINRA-supervised broker-dealer (Percent Securities, LLC, SEC CIK 0001863789, three years of compliant X-17A-5 filings) — institutional credibility most marketplaces lack

- $1.93B funded across 1,067 deals since 2018 with 801 fully repaid (AltStreet 5/29/26 ingest; 793 in Percent's 3/31/26 self-disclosure) — substantial track record across multiple credit cycles

- Deal-level Credit Snapshot rubric (10-criterion structured disclosure) on modern deals — includes overcollateralization %, cash reserve %, simple loss coverage multiple, TTM default rate

- Secondary market launched February 2026 — order book with bid/ask depth charts gives some deals genuine pre-maturity liquidity (currently ~4.3% of deals enabled)

Key limitations

- Deal-state transitions (Workout, Reperforming, Charged Off) are exposed in the investor-api but not surfaced on the public deal-page UI — material transparency gap

- Corporate Loan deals carry 25.35% distress rate vs 3.79% for Asset-Based — investors must underwrite by financing type, not at the platform aggregate

- Third-party underwriter quality varies dramatically: Aluna Partners 33.33% distress vs Percent self-underwritten 2.59% — relevant for ~31% of platform deals not underwritten by Percent itself

- Tax inefficiency — all coupon income is ordinary interest taxed at marginal rates plus 3.8% NIIT for high earners, materially eroding after-tax returns in taxable accounts

Video Review

Percent Review Video

A short video breakdown of Percent's private credit marketplace, historical performance data, workout exposure, secondary market, and the risks to understand before investing.

Where It Fits

Where Percent fits relative to the alternatives.

Marketplace direct deals

If you want

Pick your own private credit deals deal-by-deal, $500 minimums, see borrower-level data

Use

Percent marketplace — accredited investors, monthly distributions, secondary market for some deals

Managed private credit

If you want

Hands-off institutional management of a private credit portfolio with $1M+ to deploy

Use

Percent Separately Managed Accounts (1% annual fee) — built on the same deal universe

Liquid public credit exposure

If you want

Daily liquidity, no accreditation, and broader diversification across hundreds of bonds

Use

BDCs like ARCC, MAIN, or HYG / JNK high-yield bond ETFs — public market correlation tradeoff

Compare Before Deciding

Where Percent fits against alternatives

Use these hooks to pressure-test whether this is the right platform, or whether a nearby alternative matches the job better.

How this compares to EquityMultiple

EquityMultiple

Accredited-only commercial real estate platform spanning Alpine Notes, Ascent Income Fund, and EMIP equity vehicles. The Percent vs EquityMultiple guide compares private credit notes against CRE debt and equity across fees, tax reporting, liquidity, and disclosure architecture.

How this compares to Willow Wealth

Willow Wealth

Rebranded Yieldstreet multi-asset marketplace with broader asset class coverage (real estate, art, legal finance, transportation) vs. Percent's private credit focus. The Percent vs Willow Wealth guide compares the two across track record, charge-offs, regulatory history, disclosure, taxes, and liquidity.

How this compares to Cadre

Cadre

Institutional-quality commercial real estate platform for accredited investors. Complementary asset class (real estate equity vs. Percent's private credit debt) enabling cross-platform diversification but fundamentally different structure — direct property ownership vs. debt obligations, longer hold periods (5-10 years vs. 6-36 months).

Quick Answers

What most investors want to know first

The highest-signal facts first: minimums, liquidity reality, K-1 timing, and whether distributions are actually part of the experience.

Liquidity

Secondary Market launched February 2026 with order book infrastructure. Enabled on approximately 4.3% of deals as of capture date. Order-book depth, execution spreads, and completion rates are not publicly disclosed. Treat as optional upside, not primary exit path.

K-1 Timing

Default delivery is 1099-INT by January 31; K-1 for the 48 fund/SMA-structure deals may extend depending on the underlying fund close cycle.

Distributions

Monthly interest payments per the deal terms. Principal amortization begins after the initial interest-only period (typically 1-4 months from close).

Overview

Platform Overview

A concise read on what the platform is, how the structure works, and where the practical friction shows up for real investors.

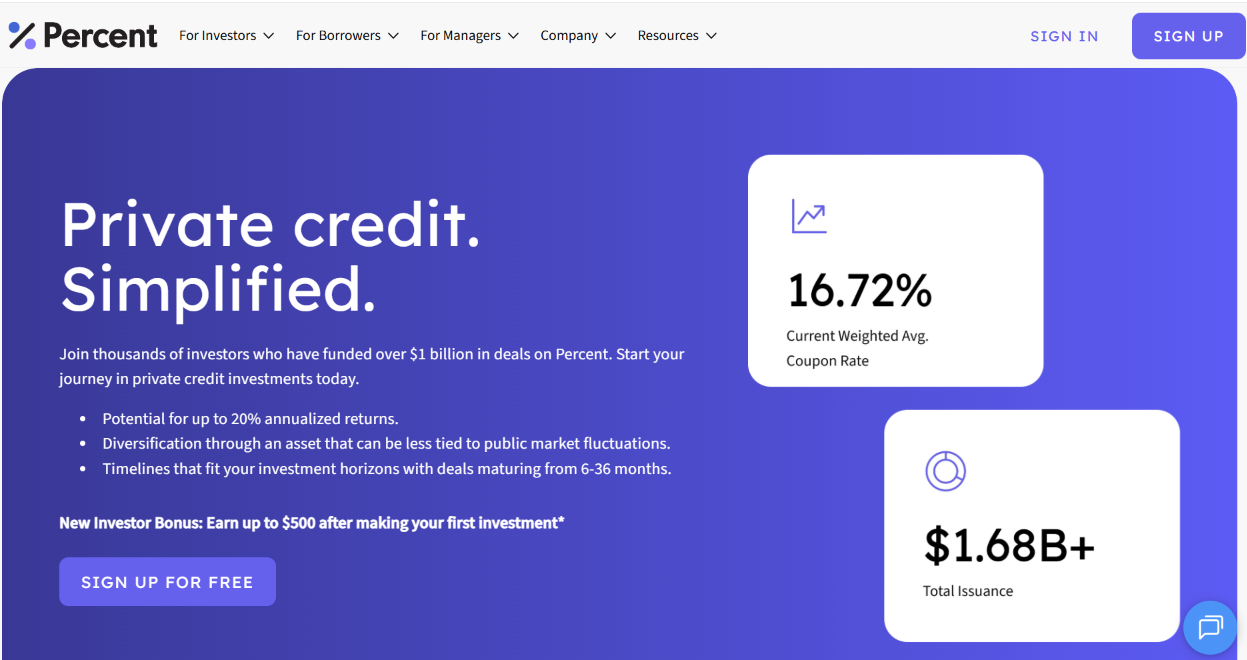

Private credit marketplace and SEC-registered broker-dealer (Percent Securities, LLC, FINRA member since August 2023, SEC CIK 0001863789) connecting 60,000+ accredited investors with short-duration alternative lending opportunities unavailable through traditional banks. Platform sources asset-based financings (consumer loans, SMB lending, merchant cash advances, discounted receivables, equipment leases, litigation finance), corporate loans, and fund structures from specialty lenders and originators worldwide, structures each deal as a dedicated Delaware Series LLC under Cadence Group Platform, LLC, and facilitates investor access through (a) the marketplace at $500 minimums per deal with self-directed allocation, or (b) Separately Managed Accounts at $1M+ minimums with 1% annual management on committed capital. Since 2018 inception through 2026-05-29, AltStreet has documented $1.93B funded across 1,067 deals — 801 fully repaid (793 in Percent's 3/31/26 self-disclosure), 193 currently outstanding, 49 in active workout, 12 charged off, 9 in active funding, 2 reperforming after prior default, 1 in pre-funding allocation. Historical weighted-average coupon: 14.76% (Percent disclosure, 3/31/26). Secondary market launched February 2026 with order book and bid/ask depth charts — currently enabled on approximately 4.3% of deals.

The platform operates as Percent Securities, LLC — an SEC-registered, FINRA-member broker-dealer (since August 2023, SEC CIK 0001863789) — and has facilitated $1.93B across 1,067 deals from December 2018 through May 2026. Investors access deals at $500 per-deal minimums via the marketplace, or delegate to professional management via Separately Managed Accounts at $1M+. Returns are paid as monthly interest at headline coupons of 10-20% (weighted-average 14.76% historical), less the platform's 10% Investor Service Fee. Default and charge-off rates are genuinely strong — 0.90% charge-off rate per Percent's own track-record disclosures, 1.17% by AltStreet's $-weighted recalculation. Secondary market launched February 2026.

Investment Structures

Marketplace ($500 per deal, self-directed) | SMA ($1M+ minimum, 1% annual management fee)

Platform Scale (AltStreet ingest 2026-05-29)

$1.93B funded · 1,067 deals · 801 repaid (AltStreet 5/29) / 793 repaid (Percent 3/31) · 123 unique borrowers · 60,000+ investors (Percent claim)

Target Returns

10-20% annual coupons · 14.76% historical weighted-average (Percent 3/31/26) · 16.95% outstanding WA coupon

Deal Duration

6-36 months typical · 9-month historical average · 17.25-month outstanding WA term (Percent 3/31/26)

Credit Performance

0.90% charge-off rate (Percent) · 1.17% $-weighted on completed (AltStreet) · 5.90% lifetime distress including workouts

Asset Types

Asset-Based ($1.62B / 870 deals) · Corporate Loans · Funds / Blended Notes

Investor Service Fee

10% of interest earned · uniform across all 549 deals where disclosed · deducted from coupon

Liquidity

Monthly interest + amortizing principal · Secondary market live since Feb 2026 (~4.3% of deals enabled)

Regulatory Status

Percent Securities, LLC — SEC-registered broker-dealer (CIK 0001863789), FINRA member since Aug 2023

Tax Document Type

1099-INT for marketplace deals (1,052 of 1,067) · K-1 for select fund/SMA structures (48 deals)

ASPrivate Credit Democratization Through Regulated Infrastructure

- Percent's broker-dealer architecture removes the structural disadvantages most private credit marketplaces face — the unregistered peer-to-peer competitors operate without FINRA suitability oversight, AML programs, or BCP requirements. The annual cost to maintain this (estimated $2M-$5M) is real, but the platform's $1.93B cumulative volume across 1,067 deals justifies the overhead.

- Short-duration focus and book-building Dutch auction price discovery enable investors to set their own yield targets — a real advantage over traditional private credit funds where the GP sets terms and you accept them. The flip side: you bear deal-selection risk that a professional manager would absorb.

- The 60,000+ investor base (per platform claims on /modern-private-credit) creates network effects: more investors → faster deal funding → more attractive economics for borrowers → more deals → more diversity for investors. Percent's competitive moat is the dual-sided network plus the regulatory wrapper most competitors lack.

- Asset-based collateral concentration ($1.62B of $1.93B = 84% by AltStreet ingest) reflects Percent's structural emphasis on recovery cushion — and the data validates this preference: Asset-Based deals show 6.7x lower distress than Corporate Loans. The platform's product-market fit is asset-backed lending, not unsecured corporate credit.

- Each deal is its own Delaware Series LLC under Cadence Group Platform, LLC — meaning your recourse in one deal is structurally isolated from problems in another. This is institutional-standard securitization architecture and protects the marketplace from contagion across deals.

Key Complexities

Deal-State Transparency Asymmetry

Percent's investor-api exposes a state field on every deal: Funding → Outstanding → Repaid OR Work-out → Charged Off / Reperforming. The marketplace UI displays Funding and Outstanding but does not foreground Work-out, Charged Off, or Reperforming on individual deal pages. An investor reviewing a borrower's prior deal that has entered workout will not see the distress flag on the deal-page view. The 49 deals currently in workout ($47.9M funded) represent 4.6% of the platform and are functionally invisible to deal-by-deal browsers. AltStreet's audit confirms zero of the 12 charged-off or 49 workout deals carry public distress disclosure in their deal-body text — the state lives only in the API.

Underwriter Quality Variance

Percent self-underwrites 68.7% of deals (733 of 1,067) and shows a 2.59% distress rate on its own book. Third-party underwriters perform very differently: Aluna Partners shows 33.33% distress (24 of 72 deals), Quiq Capital 41.67% (5 of 12), with smaller third-party underwriters varying. The underwriter is disclosed on every deal page, but the comparative quality is not. Investors must aggregate across deals manually to surface this signal. The relevance: for a Steadypay deal underwritten by Aluna Partners, the structural risk is materially higher than the platform-aggregate distress rate would suggest.

Financing Type Risk Concentration

Distress is not evenly distributed across financing types. AltStreet ingest finds Corporate Loans at 25.35% lifetime distress (36 of 142 completed-or-distressed deals) versus Asset-Based at 3.79% (27 of 712) — a 6.7x dispersion. The asset-based category itself spans SMB Financing (428 deals), Consumer Loans (215), Discounted Receivables (88), and Consumer Advances (41), with internal variance among them. An investor's effective default exposure is far more about portfolio mix than about platform-aggregate metrics.

Investor Service Fee Drag

10% of every interest payment is retained by Percent as Investor Service Fee — verified uniform across the 549 deals where disclosure could be extracted from deal body text. This is a fixed cost, not a performance fee. An 18% headline coupon nets to roughly 16.2%; a 14% coupon nets to ~12.6%. The fee is fully disclosed in each deal's Additional Details / Security Details section but is not summarized at the platform level. Investors using gross coupon for return projections systematically overstate by ~10%.

Secondary Market Maturity

Percent's Secondary Market launched February 2026 with order book and bid/ask depth charts — a structurally legitimate liquidity venue, distinct from the informal note-sale features most marketplaces offer. But it is new: only approximately 4.3% of deals are enabled (per AltStreet ingest), order-book depth is not publicly disclosed, and there is no track record of execution under stress. Practical effectiveness should be considered an emerging feature, not an established exit mechanism.

Overview Risk Notes

Credit Risk and Workout Concentration

While Percent's realized charge-off rate is genuinely strong at 0.90%, 49 deals representing $47.9M are currently in active workout — outcomes not yet realized. The lifetime distress rate including workouts and reperforming deals is 5.90% by count, 3.43% by $. Workout deal-state transitions are exposed in the investor-api but not surfaced on the public deal-page UI, creating asymmetry between platform-known and investor-visible information.

What to verify

Before investing in any deal, verify the borrower's name and check every prior deal from that borrower. Look specifically for state transitions: a borrower with prior Work-out, Reperforming, or Charged Off deals carries materially higher tail risk than the deal-page presentation suggests. AltStreet's borrower-level analysis reveals 22 active borrowers currently carry distressed prior deals — including FAT Brands (7 of 7 in workout), Juancho Te Presta (6 of 6 in workout). Treat these as elevated-risk regardless of current deal terms.

Underwriter Quality Variance

Deals underwritten by third-party originators (not Percent itself) show dramatically higher distress rates: Aluna Partners 33.33% (24 of 72 deals), Quiq Capital 41.67% (5 of 12), versus Percent self-underwritten 2.59% (19 of 733). Percent self-underwrites 68.7% of the deal book; the remaining 31% comes through third-party underwriters whose credit assessment quality varies. The underwriter is disclosed but the comparative track record is not.

What to verify

Establish a per-underwriter risk tier in your underwriting framework. Percent self-underwritten deals can carry standard sizing; Aluna Partners, Quiq Capital, and other high-distress third-party underwriters should be undersized or avoided. Cross-reference the underwriter field with AltStreet's tracked distress rates before sizing any deal. The most defensible approach is to concentrate the Percent allocation specifically in Percent-self-underwritten deals where the empirical distress rate is institutional-grade.

Tax Inefficiency in Taxable Accounts

All Percent marketplace returns are ordinary interest income (1,052 of 1,067 deals issue 1099-INT) taxed at marginal federal rates up to 37%, plus state income tax, plus 3.8% Net Investment Income Tax for AGI above $200K single / $250K married. For a high-bracket California investor: 37% fed + 13.3% state + 3.8% NIIT = 54.1% combined marginal. A 16% gross coupon nets to roughly 6.4% after federal/state/NIIT. The tax drag is structural and unavoidable in taxable accounts.

What to verify

Compute your effective after-tax return at your specific marginal bracket before sizing the allocation. High-bracket investors in high-tax states should either (a) limit Percent exposure to tax-advantaged accounts where ordinary income treatment is neutral, or (b) accept that Percent's tax-adjusted return may underperform municipal bond ladders depending on individual circumstances. Consider self-directed IRA placement through specialized custodians (Equity Trust, IRA Financial) — setup and maintenance fees are typically $200-$500 annually but become economic at $25K+ allocations.

Secondary Market Practical Effectiveness

Percent's secondary market launched February 2026 with order book and bid/ask depth — institutionally legitimate infrastructure but currently enabled on only approximately 4.3% of the deal book. Order-book depth, execution spreads, completion rates, and time-to-fill statistics are not publicly disclosed. The feature is too new to have established performance under stress.

What to verify

Underwrite every Percent deal as hold-to-maturity. Treat secondary market availability as optional upside, not a primary exit assumption. Test the feature with small positions ($500-$1,000) before depending on it for larger allocations. Maintain external liquidity (emergency reserves in liquid securities) sufficient to absorb 12-18 months of needs without forcing private credit sales. For deals where you specifically value exit optionality, verify secondary-market enablement status on the deal page before committing capital.

Limited Full-Cycle Stress Testing

Percent's deal book runs from December 2018 through May 2026 — through one mild credit disruption (COVID 2020) and the 2022-2024 rate-hike cycle, but not a sustained deep recession with simultaneous defaults. The historical 0.90% charge-off rate reflects benign macro conditions. The 49 active workouts may be an early indicator that distress is rising in the current environment, or may reflect normal noise.

What to verify

Size your Percent allocation conservatively — treat it as one component of a diversified credit allocation, not the primary credit exposure. Stress-test your portfolio assuming charge-off rates triple during recession (2.7% from current 0.90%) and recovery rates fall to 40% — both within plausible ranges based on broader private credit history. Maintain capacity to absorb a 5-10% allocation loss without forced portfolio rebalancing.

Investor Clarifications

- Verify the underwriter on every deal — Percent self-underwritten deals carry 2.59% distress, Aluna Partners-underwritten 33.33%. The underwriter is disclosed on every deal page.

- Check the borrower's prior-deal history before investing — search the borrower name and review state transitions across all prior deals. Distressed prior deals are not foregrounded on new deal pages.

- Compute the effective after-tax return at your marginal bracket — Percent's headline coupon is ordinary income, materially less tax-efficient than municipal bonds or qualified dividends for high-bracket investors in taxable accounts.

- Model returns at 90% of headline coupon — the 10% Investor Service Fee is uniform and predictable; gross-coupon modeling overstates returns systematically.

- Treat secondary market access as optional upside, not a primary exit path — the feature is new (Feb 2026), enabled on only ~4.3% of deals, with unverified order-book depth.

Mental Model

How Percent actually works — simplified.

Percent (or a third-party underwriter) sources a borrower

Most deals come from non-bank specialty lenders looking to fund their loan books — Steadypay, The Smarter Merchant, Wall Street Funding, Pollen VC, and dozens of others. Percent underwrites 68.7% of deals in-house; the rest come from third-party underwriters like Aluna Partners.

A dedicated Series LLC is formed

Each deal sits inside its own Delaware Series LLC under Cadence Group Platform, LLC (the parent's legacy name). The LLC purchases a participation interest in the borrower's underlying loans or receivables.

Investors fund the SPV through unsecured notes

You and other accredited investors buy notes issued by the Series LLC. The notes are unsecured but the SPV's claim to the underlying assets provides the structural protection. Pricing is set via Dutch auction in newer deals; rates are pre-set on older ones.

You receive monthly interest, less the 10% service fee

Cash flow from the underlying loans funds your coupon payments. Percent retains 10% of interest earned as the Investor Service Fee. After an initial interest-only period, most deals begin amortizing principal back.

The deal repays, refinances, defaults, or enters workout

Outcomes break down as: 75% repaid in full, 18% currently outstanding and performing, 5% in active workout, 1% charged off, less than 1% reperforming after recovery.

Investor Operations

The practical questions investors actually care about: when tax documents arrive, how cash distributions work, and whether capital can be exited before the underlying asset is sold.

Tax Documents

K-1 Timing

What to expect

Default delivery is 1099-INT by January 31; K-1 for the 48 fund/SMA-structure deals may extend depending on the underlying fund close cycle.

Confidence: Medium

Cash Flow

Distributions

Frequency

monthly

Timing

Monthly interest payments per the deal terms. Principal amortization begins after the initial interest-only period (typically 1-4 months from close).

Consistency

Coupon payments are contractually scheduled per each deal's terms. If a deal enters Work-out state, payment schedule may be modified or interrupted pending restructuring.

Liquidity

Exit Reality

Holding period

6-36 month deal terms typical (9-month historical average; 17.25-month outstanding WA term per Percent 3/31/26 disclosure).

Exit options

- Hold to maturity — principal returns as the underlying borrower repays the loan or as the SPV amortizes back to investors.

- Secondary Market (launched Feb 2026) — order book with bid/ask depth for ~4.3% of deals; pricing in % of par value.

- Call by the borrower — most deals callable at par + accrued interest starting from a deal-specific date (typically the 1st monthly anniversary).

Secondary market

Secondary Market launched February 2026 with order book infrastructure. Enabled on approximately 4.3% of deals as of capture date. Order-book depth, execution spreads, and completion rates are not publicly disclosed. Treat as optional upside, not primary exit path.

Confidence: Medium

Investment Structures

Asset-Based Deals (Consumer Loans, SMB Financing, Merchant Cash Advances, Discounted Receivables)

Short-duration loans (6-24 months typical) backed by underlying portfolios of consumer loans, small-business receivables, merchant cash advances, equipment leases, or discounted receivables. Represent the dominant share of platform deal flow — Percent self-reports $1.62B across 870 deals in this category (84% of platform $ volume).

Target yields 12-16% reflecting collateral backing. AltStreet ingest confirms strongest credit performance in this category: 3.79% lifetime distress (27 of 712 completed-or-distressed).

Subcategories include SMB Financing (428 deals), Consumer Loans (215), Discounted Receivables (88), Consumer Advances (41), SMB Leases (27)..

Corporate Loan Deals (Senior or Junior Direct Lending)

Senior secured or junior subordinated loans to private companies — typically 12-36 months at 16-20% headline coupons. Higher yield reflects elevated risk: AltStreet ingest finds 25.35% lifetime distress on this category (36 of 142 completed-or-distressed), 6.7x the Asset-Based rate.

The naming convention (e.g., 'Sr.' vs 'Jr.') indicates seniority; senior tranches show lower distress than junior. Investors should size Corporate Loan exposure materially smaller than Asset-Based deals — same allocation ($500-$2,500 per deal) but fewer positions in this category..

Fund Structures / Blended Notes

Diversified exposure across multiple underlying assets through a single offering — typically 36-month terms targeting 11-13% net returns with $5,000 minimums. Sold as 'Blended Notes' for marketplace investors seeking diversified entry without picking individual deals, or as fund-structure vehicles for institutional investors.

Tax document is K-1 rather than 1099-INT. AltStreet ingest finds 0% distress in this category (55 deals, all currently performing) — but the category is younger and less mature than the marketplace single-deal categories..

Separately Managed Accounts ($1M+)

Institutional-grade managed portfolios for RIAs, family offices, and accredited investors with $1M+ deploying. Percent Advisors constructs and manages the portfolio across the same deal universe with diversification by asset type, underwriter, and vintage.

Fee: 1% annual management on committed capital. Targets monthly/quarterly distributions with customizable risk parameters and mandate restrictions.

Tax document is typically K-1. Suits institutional allocators wanting outsourced operational complexity at competitive fees vs.

traditional private credit funds at 1.5-2% + carry..

Risk

Risk Structure

This is where the marketplace pitch gives way to the actual operating reality: delayed exits, limited disclosure, fee drag, and path-dependent outcomes.

Deal-State Transparency Asymmetry

Percent's investor-api exposes a state field on every deal: Funding → Outstanding → Repaid OR Work-out → Charged Off / Reperforming. The marketplace UI displays Funding and Outstanding but does not foreground Work-out, Charged Off, or Reperforming on individual deal pages. AltStreet's audit confirms zero of the 12 Charged Off or 49 Work-out deals carry public distress language in their deal-body text. The state lives only in the API. This is the central structural observation: the platform's underlying data layer contains more deal-state information than the deal-page interface surfaces.

Underwriter Quality Variance

Percent self-underwrites 68.7% of deals (733 of 1,067) and shows 2.59% lifetime distress on its own book. Third-party underwriters perform very differently: Aluna Partners 33.33% distress (24 of 72 deals), Quiq Capital 41.67% (5 of 12), with smaller third-party underwriters varying. The underwriter is disclosed on every deal page but the comparative track record is not provided. Investors filtering for Percent self-underwritten deals capture a materially lower-risk subset.

Financing Type Risk Concentration

Distress is not evenly distributed across financing types. AltStreet cross-cut: Corporate Loans 25.35% lifetime distress, Asset-Based 3.79%, Fund 0%. The 6.7x dispersion between Corporate and Asset-Based is the largest single structural risk signal in the data. Platform-aggregate metrics (0.90% charge-off rate) obscure this dispersion. Effective default exposure is far more about portfolio mix than about platform-level aggregate.

Investor Service Fee Drag

10% of every interest payment is retained by Percent as Investor Service Fee — uniform across all 549 deals where disclosure could be extracted. Fixed cost, not performance fee. Modeling at gross coupon overstates net returns by ~10%. Fully disclosed per-deal but not summarized at the platform level.

Secondary Market Maturity

February 2026 launch with order book infrastructure — structurally legitimate but enabled on only ~4.3% of deals as of capture date. Order-book depth, execution spreads, completion rates, and stress-period performance are not publicly disclosed. Practical effectiveness should be considered emerging, not established.

Limited Full-Cycle Stress Testing

Deal book runs December 2018 through May 2026 — covering COVID 2020 and the 2022-2024 rate-hike cycle but not a sustained deep recession with simultaneous defaults. Historical 0.90% charge-off rate reflects benign macro conditions. The 49 active workouts may be early signal of rising distress in the current environment, or may reflect normal noise — but the platform has not been tested under sustained credit stress.

Workouts Visible in API, Not Surfaced on Deal Pages

Risk Summary

49 deals currently in active workout state ($47.9M funded) per Percent's investor-api are not surfaced on the public deal-page UI. Workout outcomes are not yet realized — some will recover to par, some will charge off. Lifetime distress rate including workouts is 5.90% by count vs the 0.90% realized charge-off rate.

Why It Matters

Investors evaluating new deals from a borrower whose prior deals are in workout will not see that distress signal on the deal-page interface. Top 6 borrowers represent 55% of platform $ volume — concentrated dependence on a small number of large borrower relationships. Borrowers like FAT Brands (7 of 7 deals in workout), Juancho Te Presta (6 of 6 in workout), and TradeRiver (4 of 5 charged off) are visible only via deeper navigation to borrower profiles, not on deal-page views.

Mitigation / Verification

Before investing in any new deal, search the borrower's legal entity name across the platform and check the state of every prior deal. Distressed prior deals from the same borrower are a primary risk signal. Treat borrower-level concentration as a sizing input — do not over-weight a small number of large borrowers. Consider AltStreet's tracked borrower-level distress data as supplementary context when the deal-page UI is silent on prior distress.

Third-Party Underwriter Quality Dispersion

Risk Summary

Aluna Partners-underwritten deals show 33.33% distress across 72 deals; Quiq Capital 41.67% across 12 deals; Percent self-underwritten 2.59% across 733 deals. The underwriter is disclosed on every deal page but the comparative track record is not — investors must aggregate across deals manually to surface this signal. This is not a pure underwriter skill ranking because borrower mix, deal type, and sample size differ — but the dispersion is large enough to treat underwriter identity as a primary risk input.

Why It Matters

Treating all deals as having equivalent underwriting rigor would systematically understate risk on the 31% of deals not underwritten by Percent itself. Aluna Partners-underwritten deals fail at ~13x the rate of Percent-underwritten — a dispersion that's empirically large and consistent. For a borrower like Steadypay (underwritten by Aluna Partners), the structural risk profile is fundamentally different from a Percent-underwritten deal of equivalent stated terms.

Mitigation / Verification

Establish a per-underwriter risk tier in your underwriting framework. Filter for Percent self-underwritten deals where the empirical distress rate (2.59%) is institutional-grade. Treat Aluna Partners, Quiq Capital, and other high-distress third-party underwriters as elevated-risk requiring smaller position sizes or avoidance. The underwriter field is on every deal page; the relative quality is not — cross-reference with AltStreet's tracked underwriter-level distress before sizing.

Tax Inefficiency in Taxable Accounts

Risk Summary

All marketplace returns are ordinary interest income (1,052 of 1,067 deals issue 1099-INT) taxed at marginal federal rates up to 37%, plus state income tax, plus 3.8% NIIT. For a California investor at 54.1% combined marginal, a 16% gross coupon nets to roughly 7.3% after-tax — competitive with municipal bonds but far less compelling than headline numbers suggest.

Why It Matters

Investors comparing Percent's headline 14-18% coupons to municipal bond yields or qualified dividend stocks may overstate Percent's relative appeal in taxable accounts. The structure does not benefit from depreciation, 1031 exchanges, or capital gains treatment. In tax-advantaged accounts (IRA, 401k via self-directed custodians), the dynamics reverse — Percent's coupon income is fully shielded.

Mitigation / Verification

Compute your effective after-tax return at your specific marginal bracket and state of residence before sizing the allocation. High-bracket investors in high-tax states should either limit Percent exposure to tax-advantaged accounts or accept that after-tax math may underperform municipal bond alternatives. Consider self-directed IRA placement through Equity Trust or IRA Financial — setup and maintenance costs amortize over $25K+ allocations.

Credit Cycle Sensitivity and Limited Stress Testing

Risk Summary

Percent's deal book runs primarily through benign macro conditions (2018-2026 with COVID 2020 as the only meaningful stress test). The 0.90% charge-off rate reflects favorable underwriting environment. Future stress periods may show charge-off rates 2-3x current levels and reduced recovery rates.

Why It Matters

Private credit performance varies dramatically by macro environment: defaults rise, recoveries fall, secondary market liquidity evaporates during recession. Investors treating current credit metrics as a permanent baseline may be unprepared for stress-period dynamics. The 49 active workouts may be an early signal of rising distress or may reflect normal noise — the data is insufficient to distinguish.

Mitigation / Verification

Size your Percent allocation conservatively as one component of a diversified credit allocation, not the primary credit exposure. Stress-test your portfolio assuming charge-off rates triple during recession and recovery rates fall to 40%. Maintain capacity to absorb a 5-10% allocation loss without forced portfolio rebalancing.

Secondary Market Liquidity Uncertainty

Risk Summary

Secondary Market launched February 2026 with order book infrastructure but enabled on only approximately 4.3% of deals. Order-book depth, execution spreads, and completion rates are not publicly disclosed. The feature is too new to have established performance under stress.

Why It Matters

Investors viewing 'secondary market available' marketing may treat it as guaranteed pre-maturity exit and size positions accordingly. For ~95% of deals not yet enabled, no secondary exists. Even for enabled deals, thin order books could force material discounts (15-30% below par) or extended fill times — particularly during stress when multiple investors might simultaneously seek exits.

Mitigation / Verification

Underwrite every Percent deal as hold-to-maturity. Treat secondary market access as optional upside, not primary exit assumption. Test the feature with small positions before depending on it. Maintain external liquidity sufficient to absorb 12-18 months of needs without forcing private credit sales.

Biggest Misconceptions & What Actually Happens

- Verify the underwriter on every deal — Percent self-underwritten 2.59% distress vs Aluna Partners 33.33%. The underwriter is disclosed on every deal page.

- Check the borrower's prior-deal history before investing — search by borrower name and review state transitions across all prior deals. Distressed prior deals from the same borrower are not foregrounded on new deal pages.

- Compute the effective after-tax return at your marginal bracket — Percent's headline coupon is ordinary income, materially less tax-efficient than municipal bonds for high-bracket investors in taxable accounts.

- Model returns at 90% of headline coupon — the 10% Investor Service Fee is uniform and predictable.

- Treat secondary market access as optional upside, not a primary exit path — the feature is new (Feb 2026), enabled on only ~4.3% of deals.

Regulatory & Legal Posture

Security Status

Securities Offering under Regulation D (Rule 506c primarily, Rule 506b for older vintages) — Accredited Investors Only

Percent Securities, LLC is the broker-dealer entity — SEC-registered, FINRA member, registered since August 2023. SEC CIK 0001863789.

The platform has filed compliant X-17A-5 FOCUS Reports for three consecutive fiscal years (FY2023 filed 2024-02-29, FY2024 filed 2025-03-17 with amendment 2025-05-13, FY2025 filed 2026-02-27) — confirming broker-dealer in good standing per EDGAR. AML program per FINRA Rule 3310.

BCP per FINRA Rule 4370. Chief Compliance Officer: Richard Egan ([email protected], 516-668-8121).

Form CRS, Reg BI disclosures, AML program, and BCP all publicly posted on percent.com. Listed on FINRA's regulated firms directory at 145 East 57th Street, New York, NY 10022.

Modern deals (777 since 2022) use Reg D 506(c) permitting general solicitation with accredited verification; earlier vintages (274 from 2019-2021) used 506(b) with established relationships. Tax treatment: 1099-INT for marketplace structured notes (default, 1,052 deals); K-1 for select fund and SMA structures (48 deals)..

Disclosure Quality

Strong. Modern deal pages include a structured Credit Snapshot rubric (10 criteria including Overcollateralization %, Cash Reserve %, Simple Loss Coverage multiple, TTM Default Rate, Largest Obligor %, Latest Financials date, Latest Portfolio Data date), Borrower Overview, Underwriter Overview, Offering Structure, Payment Structure, Security Details, and Underlying Asset Exposure / Reporting / Risks sections. Surveillance reports posted to borrower profile pages. Investor Service Fee disclosed per-deal in Additional Details / Security Details. Critical gap: deal-state transitions (Outstanding → Work-out → Charged Off / Reperforming) are exposed in the platform's investor-api but are NOT surfaced on the public deal-page UI — material transparency observation. The state field exists; the consumer interface does not display it on individual deal views.

Custody Model

Per-Deal Delaware Series LLC under Cadence Group Platform, LLC | Investor-Owned Unsecured Notes | Percent Securities Holds Customer Funds

Regulatory Backing

Each deal sits inside its own Delaware Series LLC (137 unique Series identifiers documented across the 1,067-deal book), under the umbrella entity Cadence Group Platform, LLC (the parent's legacy name). The Series LLC purchases a participation interest in the underlying borrower's loan portfolio or receivables; investors receive unsecured notes issued by the Series LLC.

Per Percent's Business Continuity Plan (FINRA Rule 4370 required filing): Percent Securities, LLC maintains custody of customer funds and securities; in the event of significant business disruption, customers would be directed to contact issuers directly to verify the status of closings and their holdings. SPV-level recourse: investors in one Series have no claim against another Series's underlying assets — institutional-standard isolation architecture.

The notes themselves are unsecured but the SPV's participation claim against the underlying borrower's collateralized assets provides the structural recovery path. Audit/administration: Marketplace deal SPVs do not consistently disclose independent CPA audit relationships in deal body materials reviewed by AltStreet.

The parent broker-dealer entity (Percent Securities, LLC) files X-17A-5 FOCUS Reports annually as a required broker-dealer financial report, but the individual Series LLCs that hold investor notes are not separately audited per public-facing deal pages. SMA and fund structures may have separate audit relationships disclosed in offering documents.

There is no separately-named third-party fund administrator at the marketplace deal level — Percent operates as both broker-dealer and technology platform administering investor accounts, payment flows, and reporting. Custodian: Percent Securities, LLC itself per BCP disclosure — no separately-named third-party custodian holding investor assets independent of Percent Securities.

SIPC coverage applies as a FINRA-member broker-dealer with standard limitations ($500K per customer including $250K cash limit) — but SIPC does not protect against loss of value due to credit defaults on the underlying private debt; its protections are against broker-dealer insolvency and asset misappropriation only..

Tax Treatment

Reporting

1099-INT for marketplace structured notes (default, 1,052 of 1,067 deals) | K-1 for select fund / SMA structures (48 deals)

Per Percent's terms and conditions, tax forms are furnished by January 31st of the year following the calendar year to which the tax form relates (or the first business day after January 31st if it falls on a weekend or holiday), with availability through October 15th of the same year. Default cadence is straightforward 1099-INT delivery — most investors will not face K-1 timing complexity. K-1 timing for fund and SMA structures can extend into March-April or later depending on the underlying fund's financial close cycle. AltStreet's confidence on K-1 timing: medium — explicit signals on percent.com indicate variable timing for K-1 structures.

Income Character

Ordinary Interest Income (1099-INT) for Marketplace Notes | Schedule K-1 Distributions for Select Fund/SMA Structures

Marketplace deal coupons are reported as interest income on 1099-INT and taxed at marginal federal rates (10-37%) plus state income tax plus 3.8% Net Investment Income Tax for taxpayers above the AGI thresholds. There is no qualified dividend treatment, no long-term capital gains treatment on principal repayment (since these are debt instruments returning par), and no depreciation deductions.

For high-bracket investors, the effective tax rate can reach 50%+ depending on state of residence — a 16% gross coupon may net to 7-9% after-tax. For select fund and SMA structures, K-1 reporting may include passive activity income with different characterization depending on the underlying fund's tax election; consult the specific offering's tax appendix or your CPA..

Limitation

Tax inefficiency is the single largest drag on Percent's after-tax appeal for high-bracket investors. The structure does not benefit from depreciation shelter (no real assets owned), 1031 exchanges (debt instruments don't qualify), or qualified dividend rates (these are interest payments, not dividends). The standard mitigations: (a) place Percent allocations in tax-advantaged accounts (Traditional IRA, Roth IRA, 401k) through self-directed custodians like Equity Trust or IRA Financial — setup fees $50-$500, annual maintenance $100-$300, transaction fees $25-$50 per deal — typically only economic at $25K+ allocations; (b) limit taxable account exposure for high-bracket investors to a small portion of fixed-income allocation; (c) prioritize municipal bonds for the tax-efficient portion of fixed income and use Percent for the inefficient-but-higher-yield portion.

Special Considerations

- Marketplace deals report on 1099-INT — no K-1 administrative complexity for the typical investor. This is a meaningful operational advantage over many private credit alternatives that require K-1 processing.

- Net Investment Income Tax (3.8%) applies to all interest income for taxpayers with AGI above $200K single / $250K married — adds 3.8% to the effective tax burden on top of marginal federal and state rates.

- State taxation varies dramatically — Florida, Texas, Nevada, Washington, Wyoming have no state income tax (interest income taxed at federal rate only); California (up to 13.3%), New York (up to 10.9%), New Jersey (10.75%), Oregon (9.9%) impose materially higher rates. Effective state taxation determines whether Percent's after-tax return is competitive.

- Tax-advantaged account placement is the most efficient holding structure but requires self-directed IRA custodians (mainstream custodians like Fidelity, Vanguard, Schwab do not support marketplace lending platforms). Setup costs and annual maintenance need to be amortized over a sufficient allocation to be economic.

- K-1 fund/SMA structures may pass through additional tax characteristics depending on the underlying fund's elections — review each offering's tax appendix carefully if investing in the 48 non-1099-INT deals.

Before You Invest

Get Percent investor insights before you invest

K-1 timing, distribution updates, yield insights, and risk signals for Percent and similar platforms.

- Weekly platform research focused on tax timing and liquidity reality.

- Signals on distributions, risks, and structural tradeoffs before capital is locked up.

- Coverage of adjacent platforms so you can compare better options faster.

Get weekly platform signals

Track fee changes, liquidity updates, risk flags, and adjacent platforms before you invest.

Independent intelligence from AltStreet. No hype. No sponsor spin.

AltStreet Data Layer

What the data actually shows

AltStreet's authenticated ingest of all 1,067 Percent deals via the platform's /investor-api (2026-05-29) surfaces five findings that the public deal-page UI does not foreground.

49 deals are in active workout — and the deal pages don't say so

AltStreet's ingest of the /investor-api state field reveals 49 deals currently in Work-out state ($47.9M funded) and 2 in Reperforming. Combined with the 12 Charged Off deals, the lifetime distress rate is 5.90% by count. Zero of these 63 distressed deals carry distress language in their public deal-body text — the state lives only in the API.

What this means

Investors browsing the marketplace UI cannot see whether a borrower's prior deals are in workout. To assess borrower-level history, the borrower profile must be navigated to and prior-deal state inferred from indirect signals.

Corporate Loan distress is 6.7x the Asset-Based rate

AltStreet cross-cut: Corporate Loan deals show 25.35% lifetime distress (36 of 142 completed-or-distressed), Asset-Based show 3.79% (27 of 712), Fund deals show 0% (55 deals, all currently performing). The platform-aggregate 0.90% charge-off rate obscures this dispersion.

What this means

Investors should size Corporate Loan exposure materially smaller than Asset-Based exposure. A platform-aggregate sizing rule systematically over-allocates to the high-distress segment.

Third-party underwriter Aluna Partners shows 33.33% distress

AltStreet cross-cut by underwriter: Percent self-underwritten 19 of 733 distressed (2.59%); Aluna Partners 24 of 72 (33.33%); Quiq Capital 5 of 12 (41.67%); smaller third-party underwriters varying. Percent self-underwrites 68.7% of the deal book. Caveat: this is not a pure underwriter skill ranking because borrower mix, deal type, and sample size differ across underwriters.

What this means

The dispersion is large enough to treat underwriter identity as a primary risk input even after accounting for sample-size variance. Underwriter identity is disclosed on the deal-page UI but comparative track record is not contextualized — investors filtering for Percent self-underwritten deals capture a materially lower-risk subset.

Investor Service Fee is uniformly 10% — across all 549 disclosed deals

AltStreet extracted the Investor Service Fee from the deal body text for 549 of 1,067 deals. In every single case, the fee is 10% of interest earned. The remaining 518 deals (mostly older vintages) do not disclose the fee in extractable form but Percent's general practice documentation confirms the same uniform rate.

What this means

Net coupon = headline coupon × 0.90. The fee is structural and predictable. Investors modeling at gross coupon overstate returns by approximately 10%.

Top 6 borrowers represent 55% of platform $ volume

AltStreet's borrower-record ingest (123 unique borrowers, 93 Active, 30 Inactive) reveals concentrated dependence on a small number of large borrowers. Top borrowers by total funded amount include Wall Street Funding, The Smarter Merchant, Steadypay, Pollen VC, and several others. 30 borrowers are marked Inactive — meaning they have stopped raising new deals on Percent (some after losses, some after successful exit, some unknown).

What this means

Platform-level credit performance is heavily influenced by a small number of large borrower relationships. A single major borrower default could materially impact aggregate loss metrics. Investors should evaluate borrower-level concentration when building diversified portfolios.

Data as of 2026-05-29 . AltStreet review evidence layer . Public-source analysis

So What?

What to do differently because of this.

What this means

Distress is concentrated in Corporate Loans at 6.7x the asset-based rate

What to do

Maintain a meaningfully different sizing rule for Corporate Loan deals — perhaps half the typical position size — and concentrate diversification across Asset-Based deals where collateral provides recovery cushion.

What this means

The same borrower can appear in multiple deals — and earlier deals from a borrower now in workout may not surface on the new deal's page

What to do

Before investing in a new deal, search the borrower's name across the platform and check the state of every prior deal. A borrower with prior workouts deserves scrutiny even if the new deal looks clean.

What this means

Third-party underwriter quality varies materially

What to do

Aluna Partners-underwritten deals show a 33.33% distress rate (24 of 72 deals) vs 2.59% for Percent-underwritten (19 of 733). Treat the underwriter identity as a primary risk input, not a footnote.

What this means

The 10% Investor Service Fee is a fixed drag, not a variable performance fee

What to do

Model every Percent deal at 90% of headline coupon. The fee comes out whether the deal performs at target, underperforms, or workouts to par. There's no waterfall.

Decision Fit

Investor Fit

Who this works for, who it does not, and what level of patience and complexity tolerance the platform really demands.

Diversified Private Credit Allocators with $25K-$100K Available Capital

Well-suited for accredited investors building a 20-50 deal diversified private credit portfolio across multiple borrowers, financing types, and underwriters. With $25K-$100K available, an investor can construct meaningful diversification ($500-$2,500 per deal across 20-50 positions) while concentrating in Asset-Based deals where empirical distress rates are lowest.

The platform's regulatory wrapper (FINRA broker-dealer, three years of compliant X-17A-5 filings) provides institutional protections rare in this asset class. Best practice: 70% Asset-Based / 30% other financing types; favor Percent self-underwritten over third-party underwritten; verify borrower history across prior deals..

RIAs and Family Offices with $1M+ Seeking Outsourced Private Credit Management

Well-suited for RIAs, family offices, and institutional investors with $1M+ deploying via Percent's Separately Managed Account product (1% annual management on committed capital). The SMA structure delegates deal selection, monitoring, and reinvestment to Percent's investment team while providing institutional-grade reporting and dedicated relationship management.

For RIAs serving accredited clients who want private credit exposure without operational burden, the SMA wraps the marketplace's underlying deal universe in professional management — typically targeting 20-50 underlying positions with diversification across asset types and underwriters. Fee comparison: 1% management is competitive vs.

typical private credit fund 1.5-2% + carry structures..

Active Yield-Focused Investors Comfortable with Ongoing Deal Evaluation

Well-suited for accredited investors who treat private credit allocation as an active position — reviewing new deal offerings weekly, evaluating Credit Snapshot rubrics, monitoring deal-level performance, and reinvesting principal as deals repay. The marketplace requires ongoing engagement, and investors who view this as an analytical asset class (rather than passive income generation) extract the most value.

Dutch auction price discovery rewards investors who set their own yield targets rather than accepting GP-set terms. Compounding mechanics — reinvesting principal as deals repay at 6-36 month intervals — favor active monitors..

High-Income Investors in High-Tax States Seeking Maximum After-Tax Yield

Neutral fit for high-bracket investors in high-tax states (California, New York, New Jersey, Oregon). Percent's headline coupons (14-18%) are reduced by ordinary-income taxation: a California investor at 37% federal + 13.3% state + 3.8% NIIT faces a 54.1% combined marginal rate, converting 16% gross to ~7.3% net.

Municipal bond ladders (~4-5% tax-exempt) deliver competitive after-tax returns with materially better credit quality. The fit becomes attractive only with tax-advantaged account placement (self-directed IRA) or for investors whose marginal bracket is more moderate.

Run the after-tax math at your specific marginal rate before sizing..

Retirees Seeking Monthly Income Enhancement Beyond Traditional Fixed Income

Neutral fit for retired accredited investors seeking enhanced monthly income beyond Treasury / municipal yields. The 14-18% headline coupons (10-14% after Investor Service Fee and taxes) offer meaningful income enhancement, and monthly payment cadence aligns with retirement spending patterns.

However, three factors temper suitability: (a) credit risk during recession could disrupt income at the worst time for retirees with limited capacity to absorb losses; (b) ongoing reinvestment decisions as deals repay create operational burden many retirees don't want; (c) the 49 active workouts on the platform represent income interruption risk that fixed Treasury bond ladders don't carry. The SMA structure ($1M+, 1% fee) addresses operational burden but not the underlying credit risk..

Investors Below $5K Available Capital

Poor fit for investors with under $5K available capital. While Percent's $500 per-deal minimum is technically accessible, meaningful diversification requires 10-20 positions to mitigate single-deal default risk.

With $5K, an investor could fund 10 positions at $500 each — but a single default at 50% recovery loss produces 2.5% portfolio impact, while concentration at $1,500-$2,500 per deal produces 7.5-12.5% impact. Investors below $5K should accumulate larger capital before entry, or use traditional high-yield bond funds (HYG, JNK) providing instant diversification at any dollar amount.

The platform is not designed for token-allocation use; diversification requires meaningful capital..

Investors Requiring Guaranteed Near-Term Liquidity

Poor fit for investors who may need capital access within 12-18 months. While the Secondary Market launched February 2026 provides structural liquidity infrastructure (order book with bid/ask depth), it is enabled on only approximately 4.3% of deals and the order-book depth is unverifiable.

For the ~95% of deals not enabled, no secondary exists. Investors with imminent liquidity needs should maintain those funds in money market accounts, Treasury bills, or liquid securities — not in Percent positions, which should be underwritten as hold-to-maturity 6-36 month commitments.

Test the secondary market with small positions before depending on it..

Non-Accredited Retail Investors

Poor fit by regulatory requirement. Percent operates under Reg D Rule 506(c) and 506(b) — accredited investor status required ($200K annual income / $300K married, or $1M+ net worth excluding primary residence).

Non-accredited investors are prohibited from accessing the marketplace. Alternatives accessible to non-accredited investors include public BDC stocks (ARCC, MAIN), high-yield bond ETFs (HYG, JNK), and the few remaining peer-to-peer platforms with reduced minimums.

None match Percent's institutional infrastructure or deal-level transparency, but accreditation status is a hard regulatory gate..

Tradeoffs

Key Tradeoffs

The attraction of pre-IPO access is real, but every benefit comes bundled with a corresponding liquidity, transparency, or pricing cost.

Private Credit Market Scale and Growth

Morgan Stanley reports private credit as a $3.5 trillion asset class with projected growth to $5 trillion by 2029. Institutional demand from pension funds, endowments, and insurance companies has driven the asset class from niche to mainstream.

Percent's role as the accredited-retail marketplace gateway captures the segment between liquid public credit (HYG, BDCs) and institutional private credit funds (Apollo, Blackstone, Ares). Tradeoff: as more retail capital enters private credit, returns may compress and underwriting standards may loosen — the same dynamic that affected peer-to-peer lending in 2014-2018..

Regulatory Infrastructure Burden

Percent's broker-dealer registration is genuinely distinguishing — most private credit marketplace competitors operate as unregistered platforms. The annual cost to maintain broker-dealer status (estimated $2M-$5M for compliance, capital, examinations) requires substantial deal volume to justify.

The flip side: unregistered fintech competitors operate with lighter overhead and may offer cheaper deal economics, but lack FINRA supervisory framework, suitability obligations, and dispute resolution mechanisms. Investors should weigh whether the regulatory wrapper justifies any incremental cost embedded in deal economics..

Credit Cycle Sensitivity

Private credit performs best during stable-to-rising rate environments where short-duration assets repay quickly at attractive yields. Recession dynamics shift the calculus: defaults rise, recoveries fall, secondary liquidity evaporates, and originator quality variance amplifies.

Percent's $1.93B / 1,067-deal track record exists primarily during benign macro conditions (2018-present, with COVID 2020 as the only meaningful stress test). Investors should assume future stress periods may show charge-off rates 2-3x current levels and reduced recovery rates..

Originator and Underwriter Relationships

Percent's deal flow depends on relationships with non-bank originators (Steadypay, The Smarter Merchant, Pollen VC, Wall Street Funding, FAT Brands, dozens of others) and third-party underwriters (Aluna Partners, Quiq Capital, others). These relationships are commercial — originators evaluate multiple distribution channels and may shift volume away if competing marketplaces offer better economics.

The 30 inactive borrowers in AltStreet's borrower-record ingest represent borrowers who have ceased originating new deals on Percent — some left after losses, some after success, some unknown. The deal pipeline depends on continuous relationship maintenance..

Avoid

Who This Is Not For

This section should be read as a filter, not an afterthought. If you need income, simplicity, or near-term access to capital, the structure is working against you.

Non-Accredited Investors

Regulation D (506b / 506c) offerings require accredited status. Percent legally cannot accept non-accredited investors.

Alternatives: public BDC stocks (ARCC, MAIN), high-yield bond ETFs (HYG, JNK), or platforms accepting non-accredited capital under Regulation A or crowdfunding rules..

Investors Requiring Capital Access Within 12 Months

Even with the February 2026 Secondary Market launch, only approximately 4.3% of deals are enabled for secondary trading and order-book depth is unverifiable. The remaining 95% of deals are functionally hold-to-maturity.

Investors with near-term liquidity needs should keep those funds in money market accounts or short-duration Treasuries..

Tax-Sensitive High-Income Investors in High-Tax States Without IRA Capacity

All marketplace returns are ordinary interest income. For a California investor at 54.1% combined marginal, a 16% gross coupon nets to ~7.3% after-tax — competitive with municipal bonds but far less compelling than headline numbers suggest.

Without tax-advantaged account placement, the after-tax math may not justify the credit risk..

Passive Income Investors Who Won't Monitor Deal-Level Performance

The marketplace requires ongoing engagement: reviewing new offerings, monitoring deal-level state transitions (not surfaced on the UI), tracking borrower-level prior-deal history, and reinvesting principal as deals repay every 6-36 months. The SMA structure ($1M+ minimum) addresses this but requires substantially larger capital.

Passive investors with smaller capital should use BDCs or high-yield bond funds instead..

Investors With Less Than $5K Available Capital

Meaningful diversification across 10-20 deals requires $5K-$10K minimum. Concentration at $500-$2,500 per deal with too few positions creates binary exposure: a single default at 50% recovery produces disproportionate portfolio impact.

Below $5K, use traditional bond funds that diversify at any allocation size..

Risk-Averse Capital Preservation Investors

Despite strong realized charge-off rates (0.90%), private credit carries genuine principal loss risk. The 49 active workouts on the platform represent unresolved distress — some will charge off, some will recover.

Investors prioritizing absolute capital preservation should use FDIC-insured deposits, Treasury bonds, or short-duration investment-grade corporate bonds where principal-at-risk dynamics are materially different..

Editorial View

AltStreet Perspective

The compressed version of the review: what matters, what marketing tends to obscure, and how we would frame the platform for a serious allocator.

Verdict

Percent is the most institutionally-credible private credit marketplace available to accredited retail investors — SEC-registered broker-dealer, three years of compliant X-17A-5 filings, $1.93B funded across 1,067 deals, 0.90% charge-off rate that AltStreet's independent recalculation confirms. The platform has earned its position. The friction is structural: deal-state transitions like Workout (49 deals, $47.9M) exist in the underlying API but are not surfaced on the public deal-page UI. Distress concentrates dramatically by financing type (Corporate Loan 25.35% vs Asset-Based 3.79%) and by third-party underwriter (Aluna Partners 33.33% vs Percent self-underwritten 2.59%). These asymmetries are not deal-breakers — they're underwriting inputs. The investor who treats Percent as a passive private credit ETF will systematically underperform; the investor who treats it as an active asset-by-asset allocation problem will likely do well.

Positioning

AltStreet's full ingest captured all 1,067 Percent deals via the platform's authenticated /investor-api on 2026-05-29, cross-referenced with Percent's own /our-track-record-of-performance page (3/31/26), SEC EDGAR filings for Percent Securities LLC (CIK 0001863789, three years of X-17A-5 reports), FINRA broker-dealer registry, and Percent's regulatory disclosures (Reg BI, Form CRS, AML, BCP). The platform is best suited for accredited investors with $25K-$100K building a 20-50 deal diversified portfolio concentrated in Asset-Based deals (3.79% lifetime distress) underwritten by Percent itself (2.59% distress on the 733-deal self-underwritten book). The single largest underwriting mistake on this platform is treating all deals as having equivalent underwriting rigor — Aluna Partners-underwritten deals fail at 13x the rate of Percent-underwritten deals, and that variance is in the data but not foregrounded by the UI.

The Bottom Line

The deal page won't tell you it's in workout.

The API will.

Underwrite by underwriter, by financing type, and by borrower-level prior-deal history — not by platform-aggregate metrics.

Action

Next Steps

If you still want to engage after reading the review, these are the practical next moves that reduce avoidable mistakes.

Verify your accreditation status and create an account at percent.com — full marketplace access requires verification per Reg D 506(c).

Set a per-deal sizing rule before browsing offerings — $500-$2,500 per deal across 20-50 positions for a $25K-$100K allocation is the diversification baseline.

Concentrate in Asset-Based deals over Corporate Loans — the empirical distress rate dispersion (3.79% vs 25.35%) is large and consistent across vintages.

Filter for Percent self-underwritten deals — the third-party underwriter quality variance is dramatic (Aluna Partners 33.33% distress vs Percent 2.59%). The underwriter is disclosed on every deal page.

Before investing in any new deal, search the borrower name and check the state of every prior deal — distressed prior deals from the same borrower are a primary risk signal not surfaced on new deal pages.

Model returns at 90% of headline coupon — the 10% Investor Service Fee is uniform and predictable. Gross-coupon modeling systematically overstates.

Compute your effective after-tax return at your marginal bracket before sizing — Percent's tax inefficiency in taxable accounts can convert a 16% gross coupon to 7% net for high-bracket investors.

Treat the Secondary Market as optional upside, not a primary exit path — it launched Feb 2026, enabled on only ~4.3% of deals, and order-book depth is not publicly disclosed.

Final Answer

What this means for your decision.

Finding

Realized charge-off rate is 0.90% (Percent self-reported) or 1.17% by $ on completed deals (AltStreet-computed)

Meaning

The headline credit performance is low relative to many public high-yield default benchmarks (3-6% defaults typical), though methodologies are not directly comparable. Both methodologies agree the realized losses on the Percent book are low.

Action

Treat the charge-off rate as a real signal of underwriting discipline. Do not treat it as the full picture of distress on the platform.

Finding

49 deals are currently in active workout — that's 4.6% of the entire platform

Meaning

These are deals where borrowers stopped paying on schedule and are being restructured. They are exposed in the platform's investor-api but the public deal pages do not surface workout status. Workout outcomes are not yet realized — some will recover, some will charge off.

Action

When evaluating a borrower's prior deal history, check whether prior deals to the same borrower are in workout. The deal page won't tell you; the borrower-level profile may.

Finding

Corporate Loan deals show 25.35% distress rate vs. Asset-Based deals at 3.79%

Meaning

Distress is not evenly distributed across deal types. Corporate Loans concentrate distress at 6.7x the rate of Asset-Based deals. The platform-wide aggregate masks this dispersion.

Action

Underwrite Corporate Loan deals to a higher bar than asset-based deals. Do not size them equally.

Finding

Investor Service Fee is 10% of interest earned — uniform across every deal where disclosed

Meaning

Your 18% headline coupon nets to roughly 16.2% after this fee. Modeling at gross coupon overstates your return by ~10%.

Action

Always model net coupon as headline × 0.9. The fee is consistent and predictable; the math is simple.

Finding

Secondary market launched February 2026 — penetration is currently low (~4.3% of deals enabled)

Meaning

Liquidity before maturity is now technically available for a subset of deals via an order book with bid/ask depth. But the feature is new and depth is unverifiable.

Action

Underwrite every deal as hold-to-maturity. Treat secondary market access as a bonus, not a primary exit path.

If you read nothing else

Percent's credit performance is genuinely strong — 0.90% charge-offs across $1.93B funded and 1,067 deals is institutional-quality. The platform is also more transparent than most private credit competitors: 60,000+ investors, $500 minimums, monthly distributions, FINRA-supervised broker-dealer, deal-level Credit Snapshot disclosures with structured rubrics. The friction point isn't credit quality — it's that the public deal pages don't surface deal-state transitions (workout, reperforming, charge-off) that exist in the platform's underlying data. Distress doesn't equal loss, but distress is information the underlying API exposes that the consumer UI does not. Investors building a multi-deal Percent portfolio should treat that asymmetry as an underwriting input, not a deal-breaker.

Appendix

Sources, Disclosures, and Supporting Context

The lower section is structured like a report appendix: relationship context first, adjacent reading second, and evidence last.

Report Appendix

Disclosure

Relationship and compensation context

+

Report Appendix

Disclosure

Relationship and compensation context

Report Appendix

Related Resources

Adjacent platform comparisons, frameworks, and category links

+

Report Appendix

Related Resources

Adjacent platform comparisons, frameworks, and category links

Further Reading

Related Resources

Adjacent frameworks and reviews that help place the platform in a broader allocation or due-diligence context.

Explore Asset Class

Private Credit & Alternative DebtSimilar Platform Reviews

- EquityMultiple

Accredited-only commercial real estate platform spanning Alpine Notes, Ascent Income Fund, and EMIP equity vehicles. The Percent vs EquityMultiple guide compares private credit notes against CRE debt and equity across fees, tax reporting, liquidity, and disclosure architecture.

- Willow Wealth

Rebranded Yieldstreet multi-asset marketplace with broader asset class coverage (real estate, art, legal finance, transportation) vs. Percent's private credit focus. The Percent vs Willow Wealth guide compares the two across track record, charge-offs, regulatory history, disclosure, taxes, and liquidity.

- Cadre

Institutional-quality commercial real estate platform for accredited investors. Complementary asset class (real estate equity vs. Percent's private credit debt) enabling cross-platform diversification but fundamentally different structure — direct property ownership vs. debt obligations, longer hold periods (5-10 years vs. 6-36 months).

- Eagle Point Credit

Public closed-end fund (CLO equity and debt) accessible to non-accredited investors with daily liquidity vs. Percent's accredited-only marketplace. Different structure (managed fund with $0.05 minimum vs. direct deal selection at $500), different liquidity profile (daily NYSE trading vs. hold-to-maturity), but similar yield range (10-13% distribution yields historically).

Report Appendix

Evidence & Methodology

Sources, scope, and how the review was assembled

+

Report Appendix

Evidence & Methodology

Sources, scope, and how the review was assembled

ASReview Evidence

Methodology

AltStreet combined Percent's public performance disclosures with authenticated investor-api capture of deal directory, deal body, and borrower endpoints, then cross-checked regulatory status against SEC EDGAR and FINRA BrokerCheck.

Scope

Full Percent platform review covering 1,067 captured deals, 123 borrower records, 549 extracted fee-layer disclosures, Percent public track-record pages, and Percent Securities LLC regulatory filings.

AltStreet Data Layer

AltStreet full-platform ingest (capture date 2026-05-29)

AltStreet captured Percent deal directory, deal body, and borrower endpoints for all 1,067 deals as of 2026-05-29. This is a full platform credit-performance ingest, not an exit-realization database.

- Total deals captured: 1,067 (12/28/2018 → 2026-05-19 close dates)

- Total borrowers: 123 (93 Active, 30 Inactive on Percent's books)

- Lifetime funded: $1,932,813,873

- Unique underwriters / structuring agents: 29

- Average deal size: $1.81M (AltStreet denominator includes all 1,067 deals)

- Repaid: 801 deals (75.1%)

- Outstanding: 193 deals (18.1%)

- Work-out: 49 deals (4.6%, $47.9M funded)

- Charged Off: 12 deals (1.1%, $18.3M funded)

- Funding: 9 deals (0.8%)

- Reperforming: 2 deals (0.2%)

- Allocating: 1 deal (0.1%)

- Charge-off rate (count, completed only): 1.48%

- Charge-off rate ($, completed only): 1.17%

- Lifetime distress rate (CO + WO + RP / all deals): 5.90% by count, 3.43% by $

- Corporate Loan distress: 36 of 142 = 25.35%

- Asset-Based distress: 27 of 712 = 3.79%

- Percent self-underwritten distress: 19 of 733 = 2.59%

- Aluna Partners underwritten distress: 24 of 72 = 33.33%

- Quiq Capital underwritten distress: 5 of 12 = 41.67%

- Investor Service Fee: 10% of interest earned (uniform across all 549 deals where disclosed)

- Reg D 506(c): 777 deals (modern era 2022+)

- Reg D 506(b): 274 deals (2019-2021 vintages)

- Tax document: 1099-INT default (1,052 deals); K-1 for fund/SMA (48 deals)

- Secondary market enabled: ~4.3% of deals

- 137 unique Series identifiers under Cadence Group Platform, LLC

Source: AltStreet authenticated capture of Percent /investor-api (directory + body + borrower endpoints), 2026-05-29

Primary Source Pages

FAQ

Frequently Asked Questions

High-intent search questions answered directly, without making users hunt through the full review.

What is Percent and how does the private credit marketplace work?