UpMarket

UpMarket is a vertically integrated offering structure: the platform, the broker-dealer placing the deals, and several fund managers share disclosed affiliations or common control. Access Funds layer affiliated-broker fees on top of management fees, carry, and undisclosed underlying-fund fees, and the broker-dealer self-reported a net-capital deficiency to regulators.

What the data actually shows - TL;DR

UpMarket markets itself as a marketplace that 'unlocks the private markets,' but the documents describe something narrower: a vertically integrated structure in which the platform, the broker-dealer that places its deals, and several fund managers share common control. The economics reflect that integration — affiliated-broker subscription fees on every deal, layered on top of management fees, carried interest, and undisclosed underlying-fund fees.

Form D data sourced from SEC EDGAR and ingested into AltStreet's structured data layer. Coverage spans 2022-2026 across the MX/UM Pre-IPO Portfolio Fund series (I, II, III), the UM AI & Frontier Technology Fund series, and standalone Access Funds. Ownership and control findings are sourced to FINRA BrokerCheck (CRD# 295634) and the funds' own PPM conflict disclosures.

Quick Verdict

Is this platform right for you?

UpMarket is a vertically integrated alternatives platform rather than a fully independent marketplace. The platform, the broker-dealer that places its deals, and several fund managers share disclosed affiliations or common control, and the economics reflect that integration: feeder 'Access Funds' that stack an affiliated-broker subscription fee, management fee, marketing fee, and carry on top of undisclosed underlying-fund fees — with several PPMs conceding the wrapper costs more than investing directly. The broker-dealer is small and recently self-reported a net-capital deficiency. UpMarket can deliver genuine access to gated private-market exposures, but at a layered cost, through an affiliated party, and with disclosed affiliations rather than the independence its 'marketplace' framing may imply. Best for investors who specifically want a gated underlying fund they cannot otherwise reach, have read the full PPM, and accept the structure with eyes open.

Best for

- Accredited investors targeting a specific gated fund or pre-IPO name unavailable at their check size

- Investors who have read the full PPM — especially the fee stack and the 'costs more' note — and accept the related-party structure

- Investors who can independently verify the underlying third-party fund and its terms

- Long-horizon investors comfortable with multi-year illiquidity and inconsistent audit coverage

Avoid if

- You can access the underlying institutional fund directly at a lower cost

- You assumed you were using an independent, arms-length marketplace

- You need dependable income, liquidity within a defined horizon, or audited financials on every deal

- You cannot compute or accept the layered all-in cost, including undisclosed underlying-fund fees

Top strengths

- Genuine access to gated institutional funds and pre-IPO names at lower minimums

- Broad catalog across pre-IPO, crypto, private credit, hedge funds, and real estate

- FINRA-registered broker-dealer with extensive (if buried) PPM conflict and fee disclosures

- One portal for subscription, capital calls, NAV, and reporting

Key limitations

- Vertically integrated structure with disclosed affiliations or common control — not a fully arms-length marketplace

- Layered fees plus undisclosed underlying-fund fees; PPMs concede the wrapper costs more than direct

- Small broker-dealer that self-reported a 2023 net-capital deficiency

- Illiquid by design, mostly unaudited, with documented marketing-vs-PPM discrepancies

Compare Before Deciding

Where UpMarket fits against alternatives

Use these hooks to pressure-test whether this is the right platform, or whether a nearby alternative matches the job better.

How this compares to Hiive

Hiive

Live-order-book pre-IPO marketplace with disclosed bilateral commissions, 0% management fee on most Hiive Funds SPVs, and cleaner broker-dealer standing.

How this compares to EquityZen

EquityZen

Morgan Stanley-owned SPV access model with lower post-2026 buyer fees and platform-handled ROFR, useful for comparing packaged pre-IPO access.

Quick Answers

What most investors want to know first

The highest-signal facts first: minimums, liquidity reality, K-1 timing, and whether distributions are actually part of the experience.

Minimum

Marquee single-name pre-IPO funds (e.g., SpaceX/Starlink) state a $50,000 minimum on the marketing pages. Other Access Funds and feeders range from $10,000 to $100,000+ depending on the deal and share class; the products grid shows examples at $10,000 and $25,000. Minimums vary by offering, and the dossier flags at least one instance (Series K / ByteDance) where the marketed minimum ($50,000) was lower than the PPM minimum ($100,000).

Liquidity

There is no dependable secondary market for an UpMarket feeder interest. Liquidity is contingent on the underlying vehicle's terms — a venture-side exit for pre-IPO feeders, or a redemption window (subject to gates and GP discretion) for evergreen feeders. Investors should underwrite every position as effectively locked for its full stated term and longer.

K-1 Timing

K-1 timing is feeder-dependent and was not standardized in UpMarket's captured platform materials. Because most offerings are feeders into third-party funds, the UpMarket feeder must receive the underlying fund's K-1 before issuing its own, which pushes delivery later in the year. Investors should confirm expected timing in each PPM and plan accordingly rather than assuming an early-season K-1.

Distributions

Event-driven and structure-specific. Per UpMarket's FAQ, close-ended funds automatically return income, return of capital, and gains/losses to the investor's bank account on file as realizations occur; open-ended funds require a redemption request submitted through the portal, normally 2-3 months before the redemption date per the fund's rules. Pre-IPO/venture feeders should be treated as zero-yield until the underlying exits; credit and hedge-fund feeders may distribute or accrue per the underlying fund's policy.

Overview

Platform Overview

A concise read on what the platform is, how the structure works, and where the practical friction shows up for real investors.

Online investment platform and FINRA-registered broker-dealer that offers accredited investors access to private-market alternatives — pre-IPO company equity, hedge funds, private equity, private credit, crypto, and real estate — primarily through 'Access Funds,' which are feeder vehicles that invest substantially all of their assets into a single underlying third-party fund or special purpose vehicle. UpMarket and affiliated subsidiaries act as the investment manager for most Access Funds but, per the platform's own description, do not actively manage the underlying portfolios; the Access Fund simply provides a lower-minimum wrapper around an underlying institutional fund. The platform, the broker-dealer that places the offerings (UpMarket Securities LLC, f/k/a Meixin Securities LLC), and several of the fund-management entities are described in the offering documents and FINRA records as affiliated or under common control. Investors should underwrite UpMarket deals as illiquid, multi-layer private placements where a meaningful portion of capital is consumed by stacked fees before it ever reaches the underlying investment, and where the entity selecting the deal, placing the deal, and managing the wrapper are not independent of one another.

The platform's published track record is 'over $1 billion brokered for more than 1,000 investors since 2019' (stated as of December 31, 2025, and explicitly including both principal invested and appreciation). The dominant product is the 'Access Fund': a feeder vehicle that invests substantially all of its assets into a single underlying third-party fund or SPV, wrapped to offer a lower investment minimum. Per UpMarket's own FAQ, UpMarket and affiliated subsidiaries act as the investment manager for most Access Funds but do not actively manage the underlying portfolios. The structural fact that organizes everything else in this review is that UpMarket is a vertically integrated offering structure rather than a fully independent marketplace: the platform, the placement-agent broker-dealer (UpMarket Securities LLC, CRD# 295634, f/k/a Meixin Securities LLC then MX Securities LLC), and several of the fund-management entities (Aeterna Capital LLC, f/k/a UpMarket Management LLC; Meixin Management LLC; MooreBrooke Management LLC) are described in the funds' own PPM conflict disclosures and in FINRA records as affiliated or under common control. Several PPMs name Ms. Hui Chen as a control person of both the investment manager and the placement agent. The economic consequence is a layered fee structure: a typical Access Fund stacks a subscription fee (commonly ~1.5%, paid to the affiliated broker), a management fee (commonly 1% annually), a marketing fee (up to ~1%), and carried interest (commonly 10-20%) — and then passes through the underlying fund's own fees, which several PPMs decline to disclose. Multiple PPMs include a 'Special Note' stating that investing through the UpMarket fund costs more than investing in the underlying fund directly. Separately, and weighted as the substantive financial finding, UpMarket Securities LLC self-reported a net-capital deficiency (SEA Rule 17a-11) covering 01/31/2023 to 02/01/2024; its 2023 audited financials show net capital of $14,429 against an $8,749 minimum and a net loss of roughly $207,822, with two customers accounting for 68% of revenue. The firm also has two regulatory disclosure events (Alabama and Connecticut), both minor Blue Sky matters involving single sales and resolved with small consent terms or a reprimand — these are clearly separated here from the net-capital item and should not be conflated with it. AltStreet's Form D data layer documents 31 UpMarket-affiliated offerings totaling roughly $35.0M raised across about 263 investor slots (2022-2026), almost all under Rule 506(c) — a series-LLC structure whose documented growth pattern reflects frequent creation of new series vehicles alongside relatively modest individual raise sizes. UpMarket is best understood as a related-party distribution structure heavily concentrated in affiliated Access Funds: it can deliver genuine access to gated private-market exposures, but at a layered cost, through an affiliated broker, and with disclosed affiliations rather than the independence an investor might assume from the 'marketplace' framing.

Founded & Structure

Founded 2019. Online investment platform and FINRA-registered broker-dealer. Broker-dealer entity: UpMarket Securities LLC (CRD# 295634, SEC# 8-70120), f/k/a Meixin Securities LLC, f/k/a MX Securities LLC; formed in Delaware 08/09/2017, name changed from MX Securities to UpMarket Securities on 01/04/2022, SEC/FINRA-approved 05/01/2019, headquartered at 1525 McCarthy Boulevard #1000, Milpitas, CA (the affiliated management entities use a 1325 Avenue of the Americas, New York address). Ownership of the broker-dealer: the audited 2023 financials identify UpMarket Holdings, Inc. as the Sole Member at year-end 2023; FINRA BrokerCheck shows UpMarket Group Inc. as the 75%+ member effective 04/2024, with an indirect ownership chain running upward through the NGRALEAT Family LLC and NGRALEAT Family Trust (trustee Mark Li). Grace Hui Chen (CRD# 5985515 — confirmed as the 'Grace Hui Chen' named in the PPMs, distinct from a separate 'Chang-Hwa Grace Chen,' CRD# 2670708) is a registered representative of UpMarket Securities since 04/24/2020, having moved over from North Capital Private Securities Corporation (CRD# 154559) where she was registered 2019-2020. AltStreet does not assert who ultimately owns UpMarket Group Inc.; the BrokerCheck firm record documents the entity chain up through the NGRALEAT trust, and the funds' own PPMs separately name Ms. Chen as a control person of specific fund managers and the affiliated placement agent (see below).

Platform Scale (self-reported)

UpMarket states it has 'brokered over $1 billion in alternative investments for more than 1,000 investors' since 2019, measured as of December 31, 2025. The platform notes this figure includes principal invested and appreciation of investments originated via the UpMarket platform — i.e., it is a brokered-volume metric, not a net-of-fees realized return. Offerings span pre-IPO companies, hedge funds, private equity, private credit, crypto/blockchain, and real estate.

Dominant Product: Access Funds

Per UpMarket's FAQ: 'UpMarket creates Access Funds to invest directly into underlying Private Placement Funds... our Access Funds simply provide an investment structure that invests directly into the underlying Fund, but with a lower investment minimum.' UpMarket and affiliated subsidiaries act as the investment manager for most Access Funds and 'do not actively manage the underlying portfolios.' In effect, an Access Fund is a feeder: investors buy a wrapper, not an independently managed strategy.

Marquee Pre-IPO Names

Product pages and marketing feature pre-IPO exposure to names including SpaceX/Starlink, OpenAI, xAI, ByteDance, Anthropic, Databricks, Anduril, Kraken, CoreWeave, Crusoe, Lambda, Canva, Cohere, Plaid, Neuralink, and others. Exposure is typically delivered through feeder/Access Fund or co-investment structures rather than direct share ownership, and availability changes with secondary-market supply.

Investment Minimums

Marquee single-name pre-IPO funds (e.g., SpaceX/Starlink) state a $50,000 minimum on the marketing pages. Other Access Funds and feeders range from $10,000 to $100,000+ depending on the deal and share class; the products grid shows examples at $10,000 and $25,000. Minimums vary by offering, and the dossier flags at least one instance (Series K / ByteDance) where the marketed minimum ($50,000) was lower than the PPM minimum ($100,000).

Fee Structure (representative Access Fund)

Layered and deal-specific. A representative stack: Subscription fee ~1.5% of contributions (paid to the affiliated broker, UpMarket Securities); Management fee ~1% per year (charged on capital account or total subscriptions, often payable in advance, frequently waivable at the manager's sole discretion); Marketing fee up to ~1% (often carved out of contributions); Carried interest / incentive allocation commonly 10-20% (sometimes tiered with hurdles, often waivable for insiders/affiliates); PLUS a pro-rata share of the underlying fund's own management and performance fees, which several PPMs do not disclose. The platform's FAQ confirms the two most common investor fees are a subscription fee and an annual management fee.

The 'Costs More' Disclosure

Several Access Fund PPMs include a 'Special Note' stating, in substance, that investing through the UpMarket fund costs more than investing directly in the underlying fund. This is the platform's own offering documents acknowledging that the wrapper is an added cost layer. It is the single most important sentence for a prospective investor to find and read in any UpMarket Access Fund PPM.

Eligibility

US investors must be accredited; some offerings require Qualified Purchaser status (a higher threshold) or Qualified Client status. Non-US investors may invest through affiliated international entities, with eligibility determined offering-by-offering. UpMarket Securities LLC services US-based investors. Account creation is free; eligibility is enforced at the offering level.

Liquidity & Lockups

Illiquid by design. Pre-IPO and venture-feeder funds are typically locked until the underlying portfolio exits (lockups observed up to 120 months in the dataset). Evergreen credit and hedge-fund Access Funds use redemption windows with multi-month notice (commonly 1-2 year initial lockups, then quarterly or annual withdrawals subject to gates, notice periods, and GP discretion to suspend). Per UpMarket's FAQ, open-ended funds require redemption requests submitted typically 2-3 months ahead per the fund's rules; close-ended funds return capital automatically on realization.

Should You Use UpMarket?

Use it if||you specifically want exposure to a gated underlying fund or pre-IPO name you cannot otherwise reach at your check size, you have read the specific PPM in full (especially the fee stack and the 'costs more' note), you can verify the underlying fund independently, and you accept multi-year illiquidity plus a related-party structure.||Avoid it if||you assumed you were using an independent, arms-length marketplace; you cannot compute or accept the layered all-in cost; you need liquidity or audited financials on every deal; or you can access the underlying fund directly at a lower cost.

Reality Scorecard

Access to gated exposures: genuinely real. Independence of the platform from the deal economics: low — common control across platform, broker, and several managers. All-in cost transparency: low — UpMarket-level fees disclosed, underlying-fund fees frequently not. Liquidity: very low. Counterparty robustness: a concern — small broker-dealer with a recent self-reported net-capital deficiency. Audit coverage: inconsistent across deals.

Regulatory Disclosures (kept separate, and minor)

UpMarket Securities LLC has two regulatory disclosure events on its FINRA record, both Final and both minor. Alabama (initiated 11/05/2024, resolved 08/29/2025): one sale into the state where the firm believed an exemption existed; consent of a $1,000 fine plus $500 cost reimbursement and a rescission offer to the single investor. Connecticut (initiated 11/19/2020, resolved within five days): one sale to a CT resident before CT registration; resolved by filing Blue Sky paperwork, with the investor electing to remain. Neither involves fraud or investor harm. These are explicitly NOT the substantive financial item — the net-capital deficiency is — and should not be conflated with it.

Visual Summary

Outcome Scenarios

A way to underwrite the realistic range before anchoring on marquee company names or the 'over $1 billion brokered' headline.

Best case

Base case

Worst case

ASMarketplace Framing vs Underlying Structure

- The platform presents as: an independent marketplace curating the best private-market deals. The disclosed structure more closely resembles: a related-party distribution model, where the platform, the placement agent, and several managers share common control, and an affiliated broker collects a fee on every subscription. The presentation and the disclosed structure differ in ways an investor should weigh.

- Economics are materially fee-driven, not a footnote. A representative Access Fund layers a ~1.5% affiliated-broker subscription fee, ~1% annual management fee, up to ~1% marketing fee, and 10-20% carry — then passes through undisclosed underlying-fund fees. The PPMs' own 'Special Note' confirms the direct route is cheaper. The documents frame the wrapper as an access vehicle whose added cost they themselves acknowledge.

- Common control is the funds' own disclosure. Several PPMs name Ms. Hui Chen as a control person of both the investment manager and the placement agent; the manager behind the pre-IPO series was formerly named 'UpMarket Management LLC'; FINRA describes the management entities as 'under common control with the firm.' AltStreet synthesizes what the funds and FINRA already say — it does not assert beyond them.

- The broker-dealer's financial fragility is documented and material. UpMarket Securities self-reported a net-capital deficiency to regulators; its 2023 audited financials show $14,429 of net capital against an $8,749 minimum, a ~$207,822 net loss, and 68% revenue concentration in two customers. This is the substantive financial concern — distinct from, and far more important than, the two trivial Blue Sky disclosures.

- Marketing-vs-PPM gaps recur. The dossier documents Series K marketing a $50,000 minimum against a $100,000 PPM minimum, and the Adeline Berkeley EB-5 fund showing a '–' management fee in marketing against 2% in the PPM. The disciplined approach is to treat the PPM as authoritative wherever marketing materials and offering documents differ.

Key Gaps & Non-Disclosures

- Underlying-fund fees — borne pro rata, frequently 'not disclosed in this PPM.' The all-in cost cannot be computed from UpMarket's documents alone.

- Net-of-all-fees realized track record by deal and vintage. The 'over $1 billion brokered' figure includes appreciation and is a volume metric, not a per-deal net IRR.

- Audit status per deal. Most reviewed PPMs are unaudited; Life Settlement (BDO Cayman) is the exception. Audit coverage must be confirmed offering-by-offering.

- The consolidated ownership/control map in investor-facing terms. The pieces are documented across FINRA records and multiple PPMs; no single platform document presents them together for the investor.

- The universe actually shopped. 'Curated' may lead investors to assume broader market sourcing than the documents specifically describe; the documents show heavy concentration in affiliated Access Funds placed by the affiliated broker. The selection methodology is not disclosed.

Investor Operations

The practical questions investors actually care about: when tax documents arrive, how cash distributions work, and whether capital can be exited before the underlying asset is sold.

Tax Documents

K-1 Timing

What to expect

K-1 timing is feeder-dependent and was not standardized in UpMarket's captured platform materials. Because most offerings are feeders into third-party funds, the UpMarket feeder must receive the underlying fund's K-1 before issuing its own, which pushes delivery later in the year. Investors should confirm expected timing in each PPM and plan accordingly rather than assuming an early-season K-1.

Delay signals

- Feeder-into-fund structure is the default at UpMarket, and any feeder-of-a-feeder (e.g., Series K into Goanna Capital) compounds delay because each upstream layer must report first.

- Offshore underlying layers (Cayman/Luxembourg vehicles referenced in several PPMs) can extend the timeline and add reporting steps.

- Where the underlying fund is an unaffiliated third party the UpMarket manager does not control, delivery timing is outside UpMarket's control entirely.

Extension risk

For feeders into institutional underlying funds — the dominant UpMarket structure — investors should plan for a tax extension as the practical default. Standardized platform-wide guidance was not available in the captured materials; confirm per offering.

Confidence: Low

Cash Flow

Distributions

Timing

Event-driven and structure-specific. Per UpMarket's FAQ, close-ended funds automatically return income, return of capital, and gains/losses to the investor's bank account on file as realizations occur; open-ended funds require a redemption request submitted through the portal, normally 2-3 months before the redemption date per the fund's rules. Pre-IPO/venture feeders should be treated as zero-yield until the underlying exits; credit and hedge-fund feeders may distribute or accrue per the underlying fund's policy.

Consistency

No reliable platform-wide recurring distribution schedule. Cash flow depends entirely on the underlying fund's realizations and distribution policy. One marketing testimonial references real-estate funds paying ~8% annualized dividends, but that is a single offering's claim, not a platform-level income policy, and should be verified in the specific PPM.

Confidence: Medium

Liquidity

Exit Reality

Holding period

Illiquid by design and governed by the underlying vehicle. Pre-IPO/venture feeders are locked until the underlying portfolio exits (lockups up to 120 months observed in the dataset). Evergreen credit and hedge-fund feeders impose initial lockups (commonly 1-2 years) followed by redemption windows subject to notice (often 90 days), redemption caps, audit holdbacks, and GP discretion to suspend or mandatorily withdraw for any reason.

Exit options

- Realization of the underlying investment — IPO, acquisition, or fund liquidation — distributed up through the feeder to the investor.

- Redemption windows for evergreen/open-ended feeders, subject to lockups, notice periods, gates, fees, and GP discretion to suspend.

- No reliable platform-operated secondary market for feeder interests; UpMarket's own disclaimers describe the underlying as private-secondary transactions and disclaim association with the named companies.

Secondary market

There is no dependable secondary market for an UpMarket feeder interest. Liquidity is contingent on the underlying vehicle's terms — a venture-side exit for pre-IPO feeders, or a redemption window (subject to gates and GP discretion) for evergreen feeders. Investors should underwrite every position as effectively locked for its full stated term and longer.

Confidence: High

Investment Structures

Access Funds (Feeder Vehicles)

The dominant structure. A feeder LP/LLC that invests substantially all of its assets into a single underlying third-party private fund or SPV, wrapped to offer a lower minimum than the underlying fund's direct minimum.

UpMarket or an affiliated subsidiary is the investment manager but does not actively manage the underlying portfolio. Fees stack at the UpMarket level (subscription ~1.5% to the affiliated broker, management ~1% annually, marketing up to ~1%, carry commonly 10-20%) AND pass through the underlying fund's own management and performance fees, which several PPMs do not disclose.

Examples in the dataset include the SMID Biotech Access Fund (feeder into Caligan Partners), the Specialized Investment Structures Access Fund (feeder into YA Global / Yorkville), the Asset-Backed Credit Access Fund (feeder into Castlelake), the Life Settlement Access Fund (feeder into a Luxembourg securitization vehicle), and the Market Neutral Crypto Access Fund (feeder into a Monarq/MNNC master fund). Several PPMs include a 'Special Note' that investing through the fund costs more than investing directly.

Liquidity follows the underlying: locked for venture/pre-IPO feeders; redemption-window-based for evergreen credit and hedge-fund feeders, subject to lockups, notice, gates, and GP discretion to suspend..

Single-Name & Multi-Company Pre-IPO Funds

Pre-IPO exposure delivered through SPV/feeder structures rather than direct shares. Single-name funds target one company (e.g., SpaceX/Starlink, xAI, Anduril, Canva, Cohere, Crusoe, Lambda) at a stated $50,000 minimum for marquee names.

Multi-company exposure runs through series-LLC vehicles — the UM Pre-IPO Portfolio Fund I/II/III series and the UM AI & Frontier Technology Fund series — where each lettered series (A, B, C...) is a separate SPV feeding into an underlying vehicle holding the target company. Series K, for example, is a feeder-into-feeder: it invests in Goanna Capital vehicles that hold ByteDance securities, with the manager disclaiming independent verification of the underlying funds.

Carried interest on these series is commonly 20% after return of capital, with management fees ~1% and placement fees that have ranged from tiered (2%/6% by class on Series K) to flat (6% on Series R). The PPMs include the 'costs more than direct' note.

These are illiquid; lockups follow the underlying company's exit..

Co-Investment Funds

Single-asset co-investment vehicles (e.g., CoreWeave, Neuralink, ByteDance, Kraken, Plaid, Marqeta, Netskope, Databricks, Gupshup, OpenSea co-investment funds shown on the products grid) that pool investor capital alongside a lead into a specific private company position. Structurally similar to single-name SPVs, with UpMarket-level fees and reliance on the underlying position's realization for exit.

Investors should confirm the specific fee stack, the lead's terms, and the valuation basis in each PPM, as terms vary by deal..

EB-5 Immigrant-Investor Fund (Adeline Berkeley)

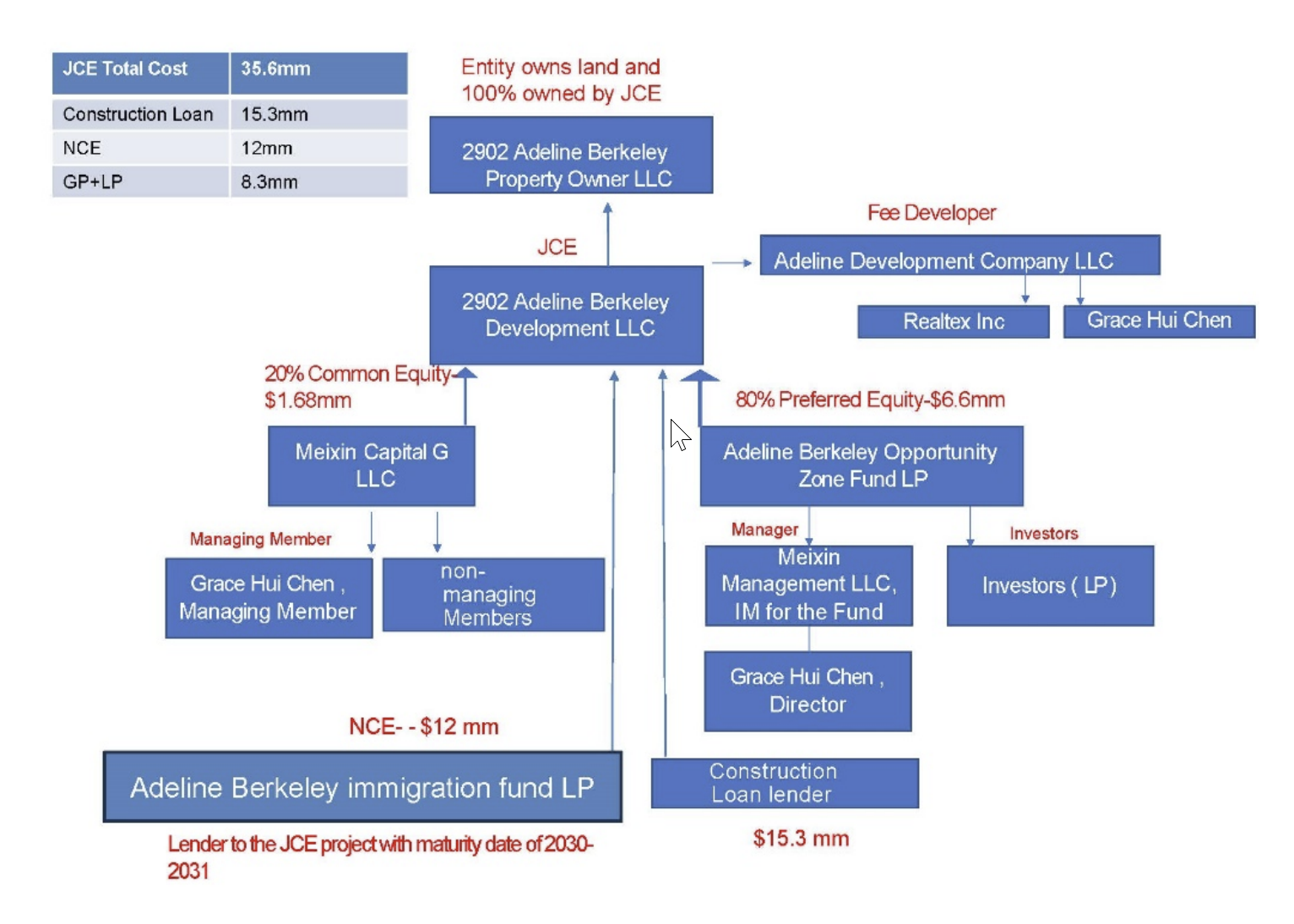

A distinct, non-securities-feeder structure, and the clearest documented example of the related-party pattern because the issuer maps it in its own PPM. The Adeline Berkeley Immigration Fund LP is the new commercial enterprise (NCE) that makes a US$12,000,000 loan to the job-creating entity (2902 Adeline Berkeley Development LLC) developing a six-story mixed-use building at 2902 Adeline Street, Berkeley, CA, for investors pursuing EB-5 permanent residency (I-526E/I-829) plus a risk-adjusted return.

The Adeline PPM's own ownership diagram shows Grace Hui Chen in three separate boxes across the structure: (1) within Adeline Development Company LLC, the fee developer (alongside Realtex Inc.); (2) as Managing Member of Meixin Capital G LLC, which holds the 20% common equity ($1.68M) in the development entity; and (3) as Director of Meixin Management LLC, the investment manager of the Adeline Berkeley Opportunity Zone Fund LP, which holds the 80% preferred equity ($6.6M). In other words, Chen-affiliated entities sit on the developer side and on both equity tranches of the borrower, while the EB-5 investors' loan sits beneath a senior construction loan.

The capital stack per the PPM diagram: total project cost ~$35.6M, senior construction loan $15.3M, NCE loan $12M, and GP+LP equity $8.3M. The PPM admits the loan terms 'were not determined by arm's length negotiations.' Fees: 2.0% annual management fee plus a flat US$80,000-per-investor administrative fee (roughly 10% of an $800,000 unit), non-refundable.

Marketing showed a management fee of '–' against the PPM's 2%. The capital is subordinate debt behind the $15.3M senior construction loan, pre-construction, with a 10-year term and no ordinary withdrawals.

A counterweight noted in the dossier: the I-956F was approved and the job-creation cushion appears sound, so the immigration feasibility is relatively strong even though the investment terms are related-party and non-arm's-length..

Risk

Risk Structure

This is where the marketplace pitch gives way to the actual operating reality: delayed exits, limited disclosure, fee drag, and path-dependent outcomes.

Vertical integration and common control

The platform, the placement-agent broker-dealer (UpMarket Securities), and several fund managers are affiliated or under common control per the funds' own PPM conflict disclosures and FINRA records. Several PPMs name Ms. Hui Chen as a control person of both the investment manager and the placement agent. The investor does not have an independent intermediary advocating against the affiliated broker and manager; the same control group selects the deal, places it, and manages the wrapper.

Layered, partially undisclosed fee stack

A representative Access Fund charges a subscription fee (~1.5% to the affiliated broker), a management fee (~1% annually), a marketing fee (up to ~1%), and carried interest (10-20%) at the UpMarket level, then passes through the underlying fund's own fees, which several PPMs do not disclose. The all-in cost is not computable from UpMarket's documents alone, and the PPMs' own 'Special Note' confirms the wrapper costs more than direct investment.

Feeder-into-feeder opacity

Many offerings are feeders into third-party funds the UpMarket manager states it does not control and has not independently verified (e.g., Series K into Goanna Capital vehicles holding ByteDance). Each layer adds fees, counterparties, and distance from the underlying asset, and the manager disclaims liability for the underlying funds' materials.

Broker-dealer financial fragility (substantive)

UpMarket Securities self-reported a net-capital deficiency (SEA Rule 17a-11) covering 01/31/2023 to 02/01/2024. The deficiency stemmed from a $28,117 restatement — a FINRA cycle exam identified expenses paid on the firm's behalf by a related party (UpMarket Group, Inc.) under an expense-sharing agreement, which had to be reclassified as a liability, reducing net capital below the minimum at various points in the period. Its 2023 audited financials show net capital of $14,429 against an $8,749 minimum (about $5,680 of cushion) at year-end, a net loss of roughly $207,822, and 68% of revenue from two customers. This is material counterparty context for an entity placing illiquid private securities and is the substantive financial finding of this review; that the breach arose from related-party expense-sharing also ties it directly to the platform's integrated structure.

Illiquidity and undefined hold periods

Pre-IPO and venture feeders are locked until the underlying exits (lockups up to 120 months observed). Evergreen credit and hedge-fund feeders use redemption windows subject to multi-month notice, gates, audit holdbacks, and GP discretion to suspend or mandatorily withdraw for any reason. Liquidity is contingent on the underlying vehicle's terms, not on UpMarket.

Marketing-vs-PPM discrepancies

The dossier documents recurring gaps: Series K marketed a $50,000 minimum against a $100,000 PPM minimum; Adeline Berkeley showed a '–' management fee in marketing against 2% in the PPM. Treat the PPM as authoritative wherever marketing materials and offering documents differ.

Inconsistent audit coverage

Most reviewed PPMs disclose unaudited financial statements; the Life Settlement Access Fund (audited annually by BDO Cayman Islands) is the noted exception. Investors should confirm audit status, administrator, and auditor per offering rather than assuming institutional-grade oversight across the platform.

Related-party structure and conflicts of interest

Risk Summary

The platform, the placement-agent broker-dealer, and several fund managers are affiliated or under common control. Several PPMs name Ms. Hui Chen as a control person of both the investment manager and the placement agent, and disclose that the manager and affiliates benefit directly from the placement and marketing fees the investor pays. Incentive allocations and management fees are frequently waivable at the manager's sole discretion and may be modified for insiders, affiliates, relatives, and strategic investors.

Why It Matters

There is no independent intermediary between the investor and the related-party complex. The same control group selects the deal, places it through its affiliated broker, and manages the wrapper, with fee waivers available to insiders that are not available to ordinary LPs. The conflict is self-disclosed but structural; it cannot be diligenced away by the investor.

Mitigation / Verification

Read each PPM's conflict-of-interest section in full and identify the named control persons and affiliated entities; confirm who receives the subscription and marketing fees; ask whether any fee waivers apply to your class versus insiders; weigh whether the access on offer genuinely justifies transacting inside a related-party structure rather than seeking the underlying fund directly.

Layered fees, including undisclosed underlying-fund fees

Risk Summary

A representative Access Fund stacks a subscription fee (~1.5%), management fee (~1% annually), marketing fee (up to ~1%), and carried interest (10-20%) at the UpMarket level, then passes through the underlying fund's own management and performance fees, which several PPMs state are borne pro rata but 'not disclosed in this PPM.' Several PPMs include a 'Special Note' that investing through the fund costs more than direct investment.

Why It Matters

The investor cannot compute the true all-in cost from UpMarket's documents alone. Layered fees compound over multi-year holds and create a meaningful net-return hurdle; the platform's own documents concede the wrapper is more expensive than the direct route for those who can access it.

Mitigation / Verification

Locate the 'Special Note' in the PPM; itemize every UpMarket-level fee; request the underlying fund's fee schedule (Annex/Appendix B references it in several PPMs); model net returns after both layers; compare against the cost of accessing the underlying fund directly if you qualify.

Broker-dealer net-capital deficiency and financial fragility

Risk Summary

UpMarket Securities LLC self-reported a net-capital deficiency (SEA Rule 17a-11) covering 01/31/2023 to 02/01/2024, identified through a FINRA cycle exam and disclosed via restatement in April 2024. The 2023 audited financials show net capital of $14,429 against an $8,749 minimum, a net loss of roughly $207,822, and 68% of revenue concentrated in two customers, with expense-sharing arrangements among commonly owned entities.

Why It Matters

The broker-dealer placing illiquid private securities is small and was recently below its regulatory net-capital floor. While this does not imply investor harm or affect the underlying investments directly, it is material counterparty and operational-stability context that the marketing's 'FINRA-registered broker-dealer' framing does not convey.

Mitigation / Verification

Review UpMarket Securities LLC's BrokerCheck report (CRD# 295634) and its most recent SEC-filed financial statements; understand that net-capital compliance is a point-in-time regulatory minimum, not a solvency guarantee; weigh the broker's size and history against the multi-year nature of the commitments it is placing.

Illiquidity and contingent exit

Risk Summary

Pre-IPO and venture feeders are locked until the underlying portfolio exits (lockups up to 120 months observed). Evergreen credit and hedge-fund feeders allow redemptions only through windows subject to 1-2 year initial lockups, 90-day-plus notice, redemption caps, audit holdbacks, and GP discretion to suspend or mandatorily withdraw for any reason. Liquidity is governed by the underlying vehicle, not UpMarket.

Why It Matters

Capital may be inaccessible for many years with no guaranteed exit. Redemption rights that look available on paper are subject to gates and GP discretion that can be exercised 'for any reason or no reason.' Time-value erodes net returns when holds extend.

Mitigation / Verification

Only commit capital you can lock up for the full stated term and longer; read the underlying fund's liquidity terms, not just UpMarket's; identify gates, notice periods, redemption fees, and suspension rights; do not treat marketed liquidity features as dependable.

Information asymmetry and limited, often unaudited disclosure

Risk Summary

Most reviewed PPMs disclose unaudited financials (Life Settlement / BDO is the exception). Exposure is typically several layers removed from the portfolio company, valuation marks rely on stale secondary prints, and the underlying funds' detailed terms are referenced in annexes rather than summarized. UpMarket's own disclaimers state that secondary-market transactions do not imply any partnership or association with the named companies.

Why It Matters

Investors make decisions on partial information about both the UpMarket wrapper and the underlying fund, with limited ongoing reporting and inconsistent audit coverage. The recognizable brand names do not translate into the disclosure quality of public securities.

Mitigation / Verification

Confirm audit status, auditor, and administrator per offering; independently research the underlying fund and manager; scrutinize the valuation basis and date; recognize that limited disclosure is inherent and accept the higher uncertainty or decline the deal.

Marketing-vs-PPM discrepancies

Risk Summary

The dossier documents recurring gaps between marketing and the controlling PPM: Series K (ByteDance) marketed a $50,000 minimum against a $100,000 PPM minimum; the Adeline Berkeley EB-5 fund showed a '–' management fee in marketing against 2% in the PPM. The pattern is consistent enough across deals to treat as a structural feature rather than isolated error.

Why It Matters

Decisions made on marketing figures can understate cost and overstate certainty. The binding terms are in the PPM, which an investor may not read closely before indicating interest.

Mitigation / Verification

Treat the PPM as authoritative on every term; reconcile each marketing figure (minimum, fees, lockup, eligibility) against the PPM before committing; if a marketing figure cannot be reconciled, ask UpMarket in writing and keep the response.

Biggest Misconceptions & What Actually Happens

- Common misconception: 'UpMarket is an independent marketplace shopping the whole market for me.' -> The platform, the broker placing the deals, and several managers share common control; the offerings are heavily concentrated in related-party Access Funds.

- Common misconception: 'An Access Fund is a managed strategy.' -> It is a feeder. UpMarket's own FAQ states it does not actively manage the underlying portfolio; you are paying for access and a lower minimum.

- Common misconception: 'The fees I see are the fees I pay.' -> The disclosed UpMarket-level fees sit on top of undisclosed underlying-fund fees; the PPMs' 'Special Note' confirms the wrapper costs more than direct.

- Common misconception: 'FINRA-registered means financially solid.' -> Registration is accurate, but the broker-dealer self-reported a net-capital deficiency and is small; registration is not a financial-strength rating.

- Typical post-investment reality: subscribe through the affiliated broker, pay the stacked entry fees, hold an illiquid feeder interest for years, receive limited reporting through the portal, and realize value only when the underlying investment exits or a redemption window opens.

Regulatory & Legal Posture

Security Status

Private placements structured as SEC Regulation D offerings (predominantly Rule 506(c), with some 506(b)), limited to accredited investors and in some cases Qualified Purchasers; placed by a FINRA-registered broker-dealer (UpMarket Securities LLC, CRD# 295634, SEC# 8-70120) that is affiliated with, or under common control with, several of the fund managers

UpMarket's offerings are private securities exempt from SEC registration under Regulation D. AltStreet's Form D data shows the offerings are overwhelmingly Rule 506(c) (general-solicitation-permitted, accredited-only) with a minority under 506(b).

Investments are structured as LP/LLC interests in feeder Access Funds or SPVs that invest into underlying third-party funds. The placement agent is UpMarket Securities LLC, a FINRA-registered broker-dealer — a fact UpMarket emphasizes in marketing — but the same broker-dealer is part of the common-control group that includes the fund managers, so its registration provides regulatory oversight without providing independence.

Reg D is a disclosure-based exemption: the protections come from the PPM disclosures (which are extensive but buried in long documents) and from accredited-investor eligibility, not from the substantive review that applies to registered offerings. Funds generally do not register under the Investment Company Act, and the PPMs disclose that disinterested-director and regulated-adviser protections are not afforded to LPs.

The substantive regulatory item on the broker-dealer's record is the self-reported net-capital deficiency (SEA Rule 17a-11, 01/31/2023-02/01/2024); two additional disclosure events (Alabama and Connecticut) are minor Blue Sky matters and are kept separate here..

Disclosure Quality

Disclosure is extensive but asymmetric and buried. The PPMs disclose the conflicts (affiliated placement agent, named control persons, fee waivers for insiders) and the layered fees at the UpMarket level — these are the funds' own words and are citable. However, the underlying funds' fees are frequently 'not disclosed in this PPM' but borne pro rata, so the all-in cost is not transparent. Most reviewed PPMs are unaudited (Life Settlement is the audited exception). The PPMs run from roughly 60 to nearly 300 pages, so the material conflict and fee disclosures, while present, require careful reading to surface. The platform-facing marketing does not consolidate the ownership/control picture and, in documented instances, understates minimums and fees relative to the controlling PPM.

Custody Model

Investors hold LP/LLC interests in an UpMarket-managed feeder (Access Fund) or SPV, which in turn holds an interest in an underlying third-party fund or SPV; UpMarket or an affiliated subsidiary acts as investment manager of the feeder but not of the underlying portfolio; third-party administrators (e.g., HC Global Fund Services LLC across several funds) and the underlying funds' custodians handle administration and custody at their respective layers; documents and NAV are accessed through the secure UpMarket portal

Regulatory Backing

The placement broker-dealer is FINRA-registered and SEC-registered, providing anti-fraud and suitability oversight, but it is affiliated with the managers and is not independent. SIPC coverage (if applicable to the broker-dealer) protects against broker-dealer failure, not investment losses.

There is no FDIC insurance. The feeder funds generally do not register under the Investment Company Act, and the PPMs disclose that Act-based protections (disinterested directors, regulated-adviser duties) are not afforded to LPs.

Investor protection rests primarily on PPM disclosure and accredited-investor eligibility, both of which are weaker than the protections attached to registered public securities..

Tax Treatment

Reporting

Schedule K-1 (Form 1065) for LP/LLC feeder and SPV interests; specific treatment is offering-dependent and should be confirmed in each PPM. UpMarket's general FAQ does not publish a standardized platform-wide K-1 timing schedule.

K-1 issuance is feeder-dependent and frequently delayed because the UpMarket feeder must wait for the underlying third-party fund's K-1 before finalizing its own. For feeders into institutional underlying funds (the dominant structure), investors should plan for late K-1 delivery and the likelihood of a tax extension. UpMarket's platform materials did not provide reliable standardized K-1 timing in the captured dossier; investors must confirm timing per offering. The UM Tax Aware Helix Fund is positioned as tax-aware, but its specific reporting mechanics should still be confirmed in its PPM.

Income Character

Pass-through partnership items reported on Schedule K-1 — capital gains on realization (commonly long-term given multi-year holds), plus interim allocations of income, gain, loss, and deduction that can include phantom income without corresponding cash

Feeder Access Funds and SPVs are taxed as partnerships, so investors report their allocable share of the underlying activity via Schedule K-1 even without cash distributions. Because most structures are feeders into third-party funds, the character and timing of income flow up from the underlying vehicle: credit and hedge-fund feeders can generate ordinary income and interim allocations annually, while pre-IPO/venture feeders typically generate little until the underlying position is realized.

Offshore underlying vehicles (several PPMs reference Cayman or Luxembourg layers) can introduce additional reporting considerations. State filing obligations may arise depending on the underlying fund's activity.

Direct EB-5 and certain debt structures (e.g., Adeline Berkeley) follow their own tax mechanics described in their PPMs. The recurring theme is that the investor's tax reporting is downstream of an underlying fund the UpMarket manager does not control, which both delays and complicates filing..

Limitation

K-1 reporting from multi-layer feeder structures is materially more complex than holding public securities and usually warrants professional tax assistance. Investors should expect delayed K-1s and likely extensions for feeders into institutional underlying funds, potential phantom income, possible offshore-related reporting, and potential multi-state filing. QSBS eligibility, if relevant, is offering-specific and depends on the underlying structure; do not assume it. Confirm all tax treatment from the actual PPM and a qualified tax adviser.

Account Suitability

Taxable

Workable but complex — K-1 reporting from feeder structures requires professional assistance; expect delayed K-1s and likely extensions; capital-gains treatment on realization is common for pre-IPO/venture feeders, while credit/hedge feeders can generate annual ordinary income and phantom-income allocations.

Roth IRA

Offered for some deals (the products grid lists 'Self-Directed IRA' and 'US / IRA / International' eligibility on certain offerings), but generally complex. Private-placement feeders in IRAs raise UBTI/UDFI considerations (especially where the underlying fund uses leverage), require a self-directed IRA custodian, and create K-1 administration inside the account. Illiquidity conflicts with RMD timing in traditional accounts. Confirm with a specialized custodian and tax adviser before using retirement accounts.

Traditional IRA

Same considerations as Roth — self-directed custodian required, UBTI/UDFI risk from leveraged underlying funds, K-1 administration inside the account, and illiquidity that conflicts with RMD obligations at 73+. Some UpMarket offerings advertise IRA eligibility, but suitability is deal-specific and should be confirmed with a specialized custodian and tax adviser.

HSA

Not suitable — HSA custodians generally do not accommodate illiquid private-placement feeders or K-1 reporting; HSA funds are intended for liquid assets and medical-expense funding.

Before You Invest

Get UpMarket investor insights before you invest

K-1 timing, distribution updates, yield insights, and risk signals for UpMarket and similar platforms.

- Weekly platform research focused on tax timing and liquidity reality.

- Signals on distributions, risks, and structural tradeoffs before capital is locked up.

- Coverage of adjacent platforms so you can compare better options faster.

Get weekly platform signals

Track fee changes, liquidity updates, risk flags, and adjacent platforms before you invest.

Independent intelligence from AltStreet. No hype. No sponsor spin.

AltStreet Data Layer

What the data actually shows

AltStreet documented 31 UpMarket-affiliated Form D offerings totaling ~$35.0M raised across ~263 investor slots (2022-2026). Key findings from the structured data layer:

A series-LLC machine, not a scaling-deal platform

17 of the 31 documented filings are lettered series (A through S) of the UM Pre-IPO Portfolio Fund II LLC, totaling ~$19.5M — each a separate SPV feeding into an underlying vehicle. The documented growth pattern reflects frequent creation of new series vehicles alongside relatively modest individual raise sizes; the average raise across all 31 filings was ~$1.13M and most were sub-$1M.

What this means

Investors should identify which specific series and underlying vehicle their deal maps to. A 'Series N' or 'Series R' is its own SPV with its own underlying fund, fee terms, and counterparty — not a share of a single diversified fund.

Activity concentrated sharply in 2025

2025 accounts for 12 of the 31 filings and ~$19.6M of the ~$35.0M total — more than half the documented capital in a single year, with 160 of the 263 investor slots. 2026 has already added 4 filings (~$2.8M) through the capture date.

What this means

The platform's offering cadence accelerated materially in 2025, consistent with the 506(c) general-solicitation model and the marquee-name marketing push (xAI, ByteDance, Vulcan Elements). Recent vintage means most positions are early in their lockups with exits years away.

Almost entirely 506(c) — built for general solicitation

29 of the 31 filings used Rule 506(c) (only two used 506(b)). 506(c) permits general advertising but requires verified accredited status, which matches UpMarket's public, marketing-forward, marquee-name acquisition model.

What this means

The 506(c) structure is why SpaceX and OpenAI can appear in public marketing at all. It also means accredited status must be verified (not merely self-certified), and that the offerings are designed to be advertised broadly rather than placed quietly to a pre-existing network.

Largest single filing: UM Tax Aware Helix Fund at $6.5M

The UM Tax Aware Helix Fund LP ($6.5M, 3 investors, 2023, 506(b)) is the largest single documented filing — and notably had only 3 investors, implying very large average checks. The next-largest filings are 2025 pre-IPO series (Series N at $4.94M/14 investors; Series P at $3.88M/12 investors).

What this means

Concentration of a $6.5M raise among 3 investors points to an institutional/UHNW subscriber base for that vehicle, distinct from the broader retail-accredited positioning. The 'Tax Aware' label signals a specific tax-management objective whose mechanics should be confirmed in the PPM.

Single-investor filings reveal bespoke / placeholder vehicles

Four filings report just one investor: Series O ($1.35M), the Adeline Berkely Immigration Fund ($800K), Series G ($250K), and Series D ($25K). Single-investor series are consistent with bespoke allocations or early/placeholder filings within the series structure.

What this means

The series-LLC framework is used flexibly — some series serve a single large investor or a specific mandate. Investors should not assume a given series is a broadly pooled, diversified vehicle without checking its actual investor count and underlying exposure.

Data as of 2026-05-25 . AltStreet review evidence layer . Public-source analysis

Full datasetDecision Fit

Investor Fit

Who this works for, who it does not, and what level of patience and complexity tolerance the platform really demands.

Accredited investors who specifically want a gated underlying fund or pre-IPO name they cannot reach directly

UpMarket can genuinely deliver a $10K-$50K ticket into institutional funds and pre-IPO names normally gated to $250K-$1M+ commitments. For an investor who has read the specific PPM, accepts the layered fees and the related-party structure, can verify the underlying fund independently, and values the access above the cost, the platform can be a reasonable tool.

The fit is neutral rather than positive because the same access often exists more cheaply via the direct route for those who qualify, and the structure is not independent..

Investors who can access the underlying institutional funds directly

The PPMs' own 'Special Note' states that investing through the UpMarket feeder costs more than investing in the underlying fund directly. An investor who already meets the underlying fund's minimum and qualification has little reason to pay the additional UpMarket subscription, management, marketing, and carry layers on top of the underlying fund's fees..

Investors who assumed they were using an independent, arms-length marketplace

The platform, the placement broker-dealer, and several managers share common control. An investor who expected an independent intermediary shopping the open market on their behalf is not getting that; the offerings are concentrated in related-party Access Funds placed by the affiliated broker.

Investors who specifically value independence should look elsewhere or accept the structure with eyes open..

Income-focused investors requiring dependable, recurring distributions

There is no platform-wide income policy. Pre-IPO/venture feeders are zero-yield until the underlying exits; credit and hedge-fund feeders distribute or accrue per the underlying fund's policy and redemption windows.

A single marketing testimonial cites ~8% real-estate-fund dividends, but that is one offering's claim, not a dependable platform feature. Not suitable for investors needing predictable cash flow..

Risk-averse investors seeking principal protection, transparency, or audited financials on every deal

Most reviewed PPMs are unaudited, underlying-fund fees are frequently undisclosed, and the underlying investments carry full loss potential. The Adeline Berkeley EB-5 fund markets 'principal protection' while being subordinate debt behind a senior construction loan on non-arm's-length terms.

Not suitable for capital preservation or for investors who require institutional-grade transparency and audit coverage across the board..

Investors requiring liquidity within a defined horizon

Lockups run from one year to a decade depending on the deal, redemption windows are subject to gates and GP discretion to suspend, and there is no dependable secondary market for feeder interests. Only suitable for capital that can remain locked for the full stated term and longer..

Tradeoffs

Key Tradeoffs

The attraction of pre-IPO access is real, but every benefit comes bundled with a corresponding liquidity, transparency, or pricing cost.

Access vs independence

UpMarket can put a small ticket into gated institutional funds and pre-IPO names — but the entity granting access is not independent of the entities collecting the fees. The platform, the placement broker, and several managers share common control..

Lower minimum vs higher all-in cost

The Access Fund wrapper lowers the dollar minimum while raising the percentage cost, stacking UpMarket-level subscription, management, marketing, and carry fees on top of undisclosed underlying-fund fees. The PPMs' own 'Special Note' confirms the direct route is cheaper..

Brand-name exposure vs information access

Recognizable names (SpaceX, OpenAI, ByteDance, Databricks) appear in marketing, but actual exposure is typically several layers removed, marked off stale secondary prints, and supported by limited, often unaudited disclosure..

Convenience vs counterparty robustness

One portal handles subscription, capital calls, and reporting — but the placing broker-dealer is small and recently self-reported a net-capital deficiency, and it sits inside the same control group as the managers..

Avoid

Who This Is Not For

This section should be read as a filter, not an afterthought. If you need income, simplicity, or near-term access to capital, the structure is working against you.

Investors who can already access the underlying institutional funds directly

The PPMs themselves state that investing through the UpMarket feeder costs more than investing directly. If you meet the underlying fund's minimum and qualification, the UpMarket layer is added cost without added value..

Investors who require an independent, arms-length intermediary

The platform, the placement broker-dealer, and several managers are affiliated or under common control, with the affiliated broker collecting a fee on every subscription. There is no independent party advocating for the investor against the related-party complex..

Income investors needing dependable recurring distributions

No platform-wide income policy exists; cash flow is event-driven and governed by each underlying fund. Pre-IPO/venture feeders are zero-yield until exit.

Not suitable for investors needing predictable income..

Investors needing liquidity within a defined horizon

Lockups run from one to ten years, redemption windows are subject to gates and GP discretion, and there is no dependable secondary market for feeder interests. Capital must be treated as locked for the full term and longer..

Investors who require audited financials and full fee transparency on every deal

Most reviewed PPMs are unaudited (Life Settlement is the exception), and underlying-fund fees are frequently undisclosed, so the all-in cost is not computable from UpMarket's documents alone..

Non-accredited investors

US offerings are limited to accredited investors, with some requiring Qualified Purchaser status. There is no access path for non-accredited US investors..

Editorial View

AltStreet Perspective

The compressed version of the review: what matters, what marketing tends to obscure, and how we would frame the platform for a serious allocator.

Verdict

A legitimate, FINRA-registered alternatives platform that provides real access to gated private-market exposures — but as a vertically integrated structure with disclosed affiliations or common control, layered fees, and a small, recently fragile broker-dealer, rather than the fully independent marketplace its framing may imply

Positioning

The platform presents as a marketplace. The disclosed structure more closely resembles a related-party distribution model. That gap is where investors can be surprised. The product grid and marquee names ('unlock the private markets,' SpaceX, OpenAI) sit atop a structure of feeder 'Access Funds' wrapped around third-party vehicles, an affiliated broker-dealer collecting a subscription fee on every deal, and fund managers that share control persons with that broker. Several PPMs name Ms. Hui Chen as a control person of both the investment manager and the placement agent; the manager behind the pre-IPO series was formerly named 'UpMarket Management' before becoming Aeterna Capital; FINRA describes the management entities as under common control with the firm. The economics follow the structure: a subscription fee, a management fee, a marketing fee, and carry at the UpMarket level, on top of undisclosed underlying-fund fees — and the PPMs' own 'Special Note' acknowledges the wrapper costs more than direct. Separately, the broker-dealer self-reported a net-capital deficiency and is small (two regulatory disclosures exist but are minor Blue Sky matters, kept distinct from the substantive net-capital finding). None of this makes UpMarket illegitimate, and the access it provides is real — for some gated exposures it may be the only practical route at a retail check size. But the suitable investor is one who reads the specific PPM in full, verifies the underlying fund independently, accepts the layered cost and the disclosed related-party affiliations, and is not relying on an independence the structure does not provide.

The Bottom Line

Real access to gated private markets, offered through an affiliated structure at a layered cost the documents themselves describe as more expensive than going direct — legitimate, but not the fully independent marketplace the framing may suggest.

Action

Next Steps

If you still want to engage after reading the review, these are the practical next moves that reduce avoidable mistakes.

Read the specific offering's PPM in full before committing — UpMarket PPMs run from roughly 60 to nearly 300 pages, and the material conflict and fee disclosures are present but buried. Prioritize the conflict-of-interest section, the fee section, and any 'Special Note.'

Find the 'costs more than direct' note and the underlying fund's fee schedule (often referenced in an annex) — then itemize every UpMarket-level fee and add the underlying-fund fees to estimate your true all-in cost.

Reconcile every marketing figure against the PPM — minimum, fees, lockup, eligibility, audit status — and treat the PPM as authoritative wherever they differ.

Verify the underlying third-party fund and manager independently — the UpMarket manager states it does not control or independently verify the underlying funds, so you must.

Review UpMarket Securities LLC's FINRA BrokerCheck (CRD# 295634) and its most recent SEC-filed financial statements to understand the placing broker-dealer's size, history, and net-capital position.

Confirm whether you could access the underlying fund directly — if you meet its minimum and qualification, the UpMarket layer may be avoidable cost.

Confirm audit status, administrator, and auditor for the specific deal — do not assume audited financials; most reviewed PPMs are unaudited.

Consult a tax adviser about feeder-structure K-1 timing (expect delays and likely extensions), phantom income, offshore-layer reporting, possible multi-state filing, and any IRA/UBTI implications if using a retirement account.

Size the position as locked for the full stated term and longer, and only commit capital you will not need before the underlying realizes or a redemption window opens.

Appendix

Sources, Disclosures, and Supporting Context

The lower section is structured like a report appendix: relationship context first, adjacent reading second, and evidence last.

Report Appendix

Disclosure

Relationship and compensation context

+

Report Appendix

Disclosure

Relationship and compensation context

Report Appendix

Related Resources

Adjacent platform comparisons, frameworks, and category links

+

Report Appendix

Related Resources

Adjacent platform comparisons, frameworks, and category links

Further Reading

Related Resources

Adjacent frameworks and reviews that help place the platform in a broader allocation or due-diligence context.

Fund Landscape

Similar Platform Reviews

- Hiive

Live-order-book pre-IPO marketplace with disclosed bilateral commissions, 0% management fee on most Hiive Funds SPVs, and cleaner broker-dealer standing.

- EquityZen

Morgan Stanley-owned SPV access model with lower post-2026 buyer fees and platform-handled ROFR, useful for comparing packaged pre-IPO access.

Report Appendix

Evidence & Methodology

Sources, scope, and how the review was assembled

+

Report Appendix

Evidence & Methodology

Sources, scope, and how the review was assembled

ASReview Evidence

Methodology

Forensic review synthesized from primary sources: (1) UpMarket platform materials captured May 20, 2026 — homepage, About, FAQ, products grid, and individual pre-IPO opportunity pages (SpaceX/Starlink, xAI, ByteDance, Unitree, Impulse Space, and others); (2) the private placement memoranda for eleven UpMarket and affiliated Access Funds, as summarized in AltStreet's deal-level dossier (Market Neutral Crypto, UM Blockchain, a16z Access, Series K/ByteDance, Adeline Berkeley EB-5, Series R/Vulcan Elements, UM Tax Aware Helix, SMID Biotech, Specialized Investment Structures, Asset-Backed Credit, and Life Settlement Access Funds); (3) FINRA BrokerCheck firm and individual records (UpMarket Securities LLC, CRD# 295634; associated individuals); (4) SEC-filed audited broker-dealer financial statements (2023); and (5) SEC EDGAR Form D filings ingested into AltStreet's structured data layer. Analysis focuses on the platform's structure and independence, fee architecture, common-control and conflict-of-interest disclosures, broker-dealer financial condition, liquidity and tax mechanics, and investor suitability. Claims are tied to the funds' own offering disclosures, FINRA/SEC records, or platform-published materials; assertions that could not be sourced to those documents are not made. Note: UpMarket gates most operational and offering detail behind account login, so the platform scrape is thinner than the PPM and regulatory record; tax-timing and some operational fields are therefore confirmed at the offering level rather than platform-wide.

Scope

Platform structure and degree of independence; ownership and common-control chain; Access Fund (feeder) mechanics; fee architecture at the UpMarket level and the treatment of underlying-fund fees; the 'costs more than direct' disclosure; broker-dealer registration and 2023 financial condition (net-capital deficiency); the two minor regulatory disclosures (kept separate); eligibility; liquidity and lockup mechanics; tax/K-1 considerations for feeder structures; marketing-vs-PPM discrepancies; the Form D data layer; and investor suitability across profiles.

Key Findings

- *PLATFORM-CONFIRMED: UpMarket states it has 'brokered over $1 billion in alternative investments for more than 1,000 investors' since 2019, as of December 31, 2025, explicitly including principal invested AND appreciation — a brokered-volume metric, not a net-of-fees return (upmarket.co FAQ and product pages).

- *PLATFORM-CONFIRMED: Access Funds are feeders. UpMarket's FAQ states it 'creates Access Funds to invest directly into underlying Private Placement Funds' with a 'lower investment minimum,' and that 'UpMarket and affiliated subsidiaries act as the Investment Managers for most of the Access Funds. We do not actively manage the underlying portfolios.'

- *PLATFORM-CONFIRMED: The two most common investor fees are a subscription fee (charged at first investment) and an annual management fee, per the FAQ; fees 'vary by each investment.' Marquee single-name pre-IPO funds (e.g., SpaceX/Starlink) state a $50,000 minimum; the products grid shows other offerings at $10,000 and $25,000.

- *PLATFORM-CONFIRMED: Eligibility is accredited-only for US investors, with some offerings requiring Qualified Purchaser status; non-US investors invest through affiliated international entities; UpMarket Securities LLC services US-based investors (FAQ).

- *PPM-SOURCED: A representative Access Fund stacks a subscription fee (~1.5%, to the affiliated broker), a management fee (~1% annually), a marketing fee (up to ~1%), and carried interest (10-20%), then passes through the underlying fund's own fees, which several PPMs state are borne pro rata but 'not disclosed in this PPM.'

- *PPM-SOURCED: Several PPMs include a 'Special Note' stating that investing through the UpMarket fund costs more than investing directly in the underlying fund.

- *PPM-SOURCED: Multiple PPMs name Ms. Hui Chen as a control person of both the investment manager and the placement agent (e.g., UM Tax Aware Helix and SMID Biotech name her explicitly), and disclose that manager/affiliates benefit directly from the placement and marketing fees — a self-disclosed conflict of interest.

- *PPM-SOURCED: Series K (ByteDance) is a feeder-into-feeder via Goanna Capital vehicles holding ByteDance securities; the manager (Aeterna Capital, f/k/a UpMarket Management) states it does not control and has not independently verified the underlying funds and disclaims liability for their materials.

- *PPM-SOURCED (issuer's own diagram): The Adeline Berkeley EB-5 fund's PPM includes an ownership diagram that places Grace Hui Chen in three separate roles — within the fee developer (Adeline Development Company LLC), as Managing Member of Meixin Capital G LLC (20% common equity, $1.68M), and as Director of Meixin Management LLC, the IM of the Opportunity Zone Fund holding the 80% preferred equity ($6.6M). The EB-5 investors' $12M loan is subordinate to a $15.3M senior construction loan (total project ~$35.6M). The PPM admits loan terms 'were not determined by arm's length negotiations'; fees include a 2% annual management fee and a flat US$80,000-per-investor administrative fee. This issuer-drawn diagram is the most direct documentation of the related-party pattern in the dataset.

- *FINRA-SOURCED: UpMarket Securities LLC (CRD# 295634), f/k/a Meixin Securities LLC and MX Securities LLC, is owned by a single member — UpMarket Holdings, Inc. per the audited 2023 financials (Sole Member at year-end 2023); UpMarket Group Inc. per BrokerCheck effective 04/2024 — with an indirect chain running up through the NGRALEAT Family LLC and NGRALEAT Family Trust (trustee Mark Li). FINRA's firm record describes UpMarket Management LLC (CRD# 336095) and Meixin Management LLC (CRD# 285614) as 'under common control with the firm,' with Robert Daniels serving as CCO of both UpMarket Securities and Meixin Management. The firm BrokerCheck does not name any individual as owner of the parent; AltStreet does not assert ultimate ownership of UpMarket Group Inc.

- *FINRA-SOURCED (identity confirmed): Grace Hui Chen holds CRD# 5985515 and is confirmed as the 'Grace Hui Chen' named in the PPMs, distinct from a separate 'Chang-Hwa Grace Chen' (CRD# 2670708). Her individual BrokerCheck shows her as a registered representative of UpMarket Securities since 04/24/2020 (prior firm: North Capital Private Securities Corporation, CRD# 154559, 2019-2020) and discloses one pending customer dispute initiated 02/15/2023 — a pending matter is an unproven allegation and is treated as such (and is not featured as a finding in this review).

- *SEC-SOURCED (substantive, verified against the 2023 audited filing): UpMarket Securities LLC self-reported a net-capital deficiency (SEA Rule 17a-11) covering 01/31/2023 to 02/01/2024, disclosed via a 04/26/2024 financial notification to FINRA and the SEC. The deficiency arose from a $28,117 restatement — a FINRA cycle exam identified expenses a related party (UpMarket Group, Inc.) paid on the firm's behalf, reclassified as a liability (Notes 4 and 8). Year-end 2023 net capital was $14,429 against an $8,749 minimum ($5,680 excess; Note 3 and the supplementary schedule); net loss was $207,822 (Statement of Operations); two customers accounted for 51% and 17% (68%) of revenue (Note 5). Auditor: BDG-CPAs, PC (PCAOB-registered), serving as the firm's auditor since 2019. This filing pertains solely to the placement-agent broker-dealer (UpMarket Securities LLC) and not to any individual fund issuer; the fund LLCs are separate entities.

- *FINRA-SOURCED (minor, kept separate): Two regulatory disclosure events, both Final and both minor Blue Sky matters — Alabama (one sale; $1,000 fine + $500 costs + rescission offer; resolved 08/29/2025) and Connecticut (one sale before registration; resolved within five days by filing Blue Sky paperwork). Neither involves fraud or investor harm; both are distinct from the net-capital finding.

- *PPM-SOURCED: Audit coverage is inconsistent — most reviewed PPMs disclose unaudited financials; the Life Settlement Access Fund is the noted exception (audited annually by BDO Cayman Islands). HC Global Fund Services LLC appears as administrator across several funds.

- *IDENTITY (resolved): The earlier dossier caution — that CRD# 5985515 'HUI CHEN' had to be confirmed as the 'Grace Hui Chen' of the PPMs and distinguished from 'CHANG-HWA GRACE CHEN' (CRD# 2670708) — has been resolved against her individual FINRA BrokerCheck record. CRD# 5985515 is Grace Hui Chen. AltStreet names her per the funds' own PPM disclosures and the issuer's own Adeline ownership diagram, and does not assert any ownership interest in UpMarket Group Inc. that is not independently documented.

- *DATA-LAYER: AltStreet documented 31 UpMarket-affiliated Form D offerings totaling ~$35.0M raised across ~263 investor slots (2022-2026); 29 of 31 under Rule 506(c); largest single filing was the UM Tax Aware Helix Fund at $6.5M; activity concentrated in 2025 (12 filings, ~$19.6M).

Primary Source Pages

FAQ

Frequently Asked Questions

High-intent search questions answered directly, without making users hunt through the full review.

What is UpMarket and how does it work?

UpMarket (founded 2019) is an online investment platform and FINRA-registered broker-dealer that offers accredited investors access to private-market alternatives — pre-IPO equity, hedge funds, private equity, private credit, crypto, and real estate. Most offerings are 'Access Funds': feeder vehicles that invest substantially all of their assets into a single underlying third-party fund or SPV, wrapped to offer a lower minimum. UpMarket states it does not actively manage the underlying portfolios; you are paying for access and a lower minimum, not for active management at the UpMarket level.

Is UpMarket an independent marketplace?

Not fully, in the arms-length sense. Per the funds' own PPM conflict disclosures and FINRA records, the platform, the placement-agent broker-dealer (UpMarket Securities LLC), and several fund managers (Aeterna/UpMarket Management, Meixin Management, MooreBrooke Management) are affiliated or under common control. Several PPMs name Ms. Hui Chen as a control person of both the investment manager and the placement agent. The offerings are heavily concentrated in affiliated Access Funds placed by the affiliated broker. Investors should weigh those disclosed affiliations rather than assume a fully independent intermediary is shopping the open market on their behalf.

What fees does UpMarket charge?

Fees are layered and deal-specific. A representative Access Fund charges a subscription fee (commonly ~1.5%, paid to the affiliated broker), an annual management fee (commonly ~1%), a marketing fee (up to ~1%), and carried interest (commonly 10-20%) — all at the UpMarket level. On top of that, the underlying third-party fund charges its own management and performance fees, which several PPMs state are borne pro rata but are 'not disclosed' in the UpMarket PPM. Several PPMs include a 'Special Note' stating that investing through the UpMarket fund costs more than investing directly in the underlying fund. Always read the specific PPM for the complete fee stack.

What is an UpMarket 'Access Fund'?

An Access Fund is a feeder. Per UpMarket's own FAQ, it 'invests directly into the underlying Fund, but with a lower investment minimum,' and UpMarket does not actively manage the underlying portfolio. So you are buying a wrapper around an underlying institutional fund or SPV, not an independently managed strategy. Some Access Funds are even feeders-into-feeders (e.g., Series K invests in Goanna Capital vehicles that hold ByteDance), which adds further layers of fees and counterparties.

What are UpMarket's minimum investment requirements?

Minimums vary by offering. Marquee single-name pre-IPO funds (such as SpaceX/Starlink) state a $50,000 minimum on the marketing pages. Other Access Funds and feeders range from $10,000 to $100,000+ depending on the deal and share class; the products grid shows examples at $10,000 and $25,000. Note that minimums in marketing have, in at least one documented case (Series K / ByteDance), been lower than the minimum stated in the controlling PPM ($50,000 marketed vs. $100,000 in the PPM) — confirm the minimum in the PPM before committing.

Who can invest on UpMarket?